Chainlink is the infrastructure everyone in tokenization swears by. The “industry standard oracle.” The bridge between blockchains. The partner of SWIFT, DTCC, and Amundi.

I went looking for the numbers behind the narrative. What I found is a company that secures $63 billion in assets, trades at a 100x price-to-sales ratio, and has been piloting with SWIFT for eight years without a single dollar of production revenue.

Let me walk you through it.

What Chainlink actually does

If you are not technical, here is the simple version. Blockchains cannot access real-world data on their own. They do not know the price of gold, the weather in Texas, or whether a bank wire landed. Chainlink provides that data. It is a network of nodes that feeds external information into smart contracts.

Think of it as a translator. The real world speaks one language. Blockchains speak another. Chainlink sits in the middle.

This matters for tokenization because if you tokenize a building, someone needs to feed the current property value into the blockchain. If you tokenize an energy storage unit, someone needs to feed the electricity price. That someone is usually Chainlink.

They also built CCIP (Cross-Chain Interoperability Protocol), which moves tokens and data between different blockchains. And CRE (Chainlink Runtime Environment), which automates workflows. But the core business is simple: data in, data out.

The good: market dominance is real

Chainlink's market position is not debatable. They secure roughly $63 billion in assets across DeFi. That is 62% of the oracle market. On Ethereum, they handle 83% of all oracle-supported value. On Base, it is close to 100%.

Their data feeds are battle-tested. Over 2,000 price feeds running across 40+ blockchains. When Aave or Compound need to know the price of ETH, they ask Chainlink. This has been the case for years.

CCIP processed $18 billion in cross-chain transfers in Q1 2026 alone. Volume grew 78% quarter over quarter and 319% year over year. When people move large amounts of value between chains, they increasingly use Chainlink.

In April 2026, Deloitte completed a SOC 2 Type 2 audit on Chainlink's infrastructure. Combined with their SOC 2 Type 1 and ISO 27001 certifications, they are the only oracle provider with all three. For institutions that need compliance checkboxes before touching crypto infrastructure, this matters.

And there are real projects using Chainlink for real-world assets. Amundi and Spiko launched a tokenized fund (SAFO) that reached $400 million in assets within three weeks. It uses Chainlink for automated NAV reporting. DTCC is building a collateral management platform on Chainlink, targeting production in Q4 2026.

These are not vaporware. They are the real deal.

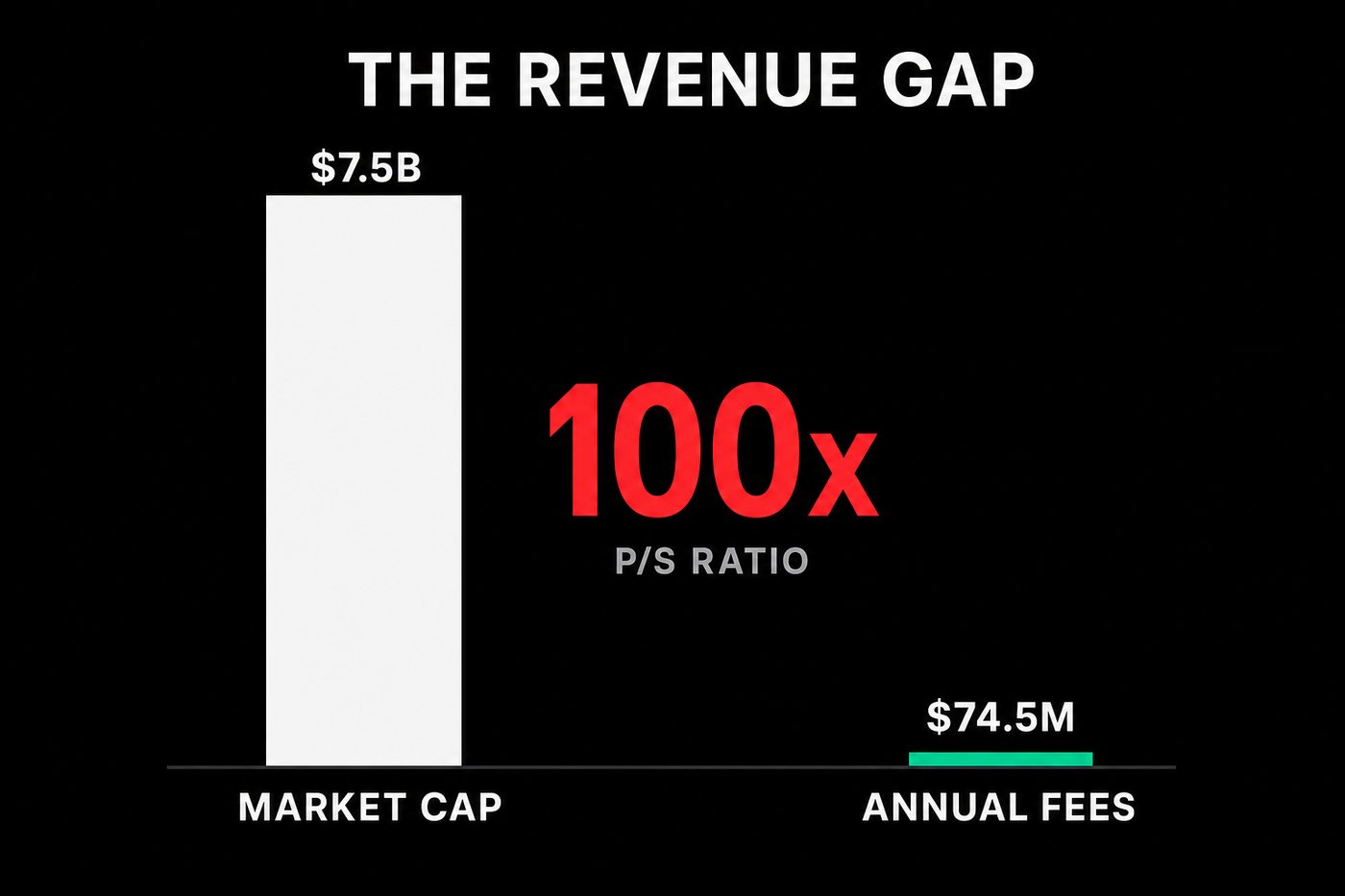

The bad: a 100x revenue multiple

Now for the part that makes me uncomfortable.

Chainlink's market cap is $7.5 billion. According to DefiLlama, its combined on-chain fees across all services — price feeds, CCIP, VRF, Keepers — total approximately $74.5 million annualized.

For a data relay service, that is a price-to-sales ratio of 100x. Not a social network. Not a cloud platform. A data relay.

Break it down further and it gets worse. CCIP processed $18 billion in Q1 2026 volume. Cumulative fees collected across CCIP's entire lifetime total roughly $603,000. That is a take rate of 0.003%. Three thousandths of a percent.

The company also claims off-chain enterprise revenue, but the “Chainlink Reserve” that supposedly converts this revenue into LINK tokens is not publicly auditable. We do not know how much flows in, how it gets converted, or where it goes. For a project built on transparency and verifiability, this is worth questioning.

The SWIFT problem

Every year since 2018, Chainlink has announced something with SWIFT. Proof of concept. Phase 1. Phase 2. “Production-grade” systems. Partnership expansion. Integration milestone.

It is now 2026. SWIFT settles $150 trillion annually. The amount of that flowing through Chainlink in production: zero.

Not low. Zero.

Twenty-four financial institutions are “participating” in various pilots and phases. Not one has committed to a binding production timeline. SBI, JPMorgan, UBS, WisdomTree — all “participants.” All piloting. Year after year.

I am not saying these partnerships are fake. They are real relationships with real institutions. But the gap between “partnership announced” and “revenue generated” is measured in years, and the counter has not started yet.

If I presented an investment deal to my investors and said “we have been piloting with the customer for eight years but have not collected a single euro in production revenue,” they would walk out of the room.

The LayerZero windfall

Chainlink's biggest growth story in May 2026 was not their own innovation. It was a competitor getting hacked.

On April 18, North Korea's Lazarus Group exploited KelpDAO through a vulnerability in LayerZero's verification system. The attack stole approximately $292 million worth of rsETH. The root cause: KelpDAO was using LayerZero with a single verifier (a “1/1 DVN” configuration), and attackers compromised that one point of failure.

Within weeks, over $1 billion in confirmed protocol value migrated from LayerZero to Chainlink's CCIP. Solv Protocol moved $700 million in tokenized bitcoin. Re Protocol moved $475 million. Multiple additional protocols followed. Some reports cite $2 billion in total migration, though the confirmed figure is closer to $1.2 billion.

This is good for Chainlink. Their multi-validator security model genuinely prevents this kind of attack. CCIP was designed so that no single compromised node can forge transactions.

But let me be clear about what happened: Chainlink did not win this business through product innovation or marketing. They won it because the alternative caught fire. LayerZero later admitted it “made a mistake” by allowing its DVN to act as a sole verifier for high-value transactions. If LayerZero patches their verification model and rebuilds trust, some of these protocols may switch back.

The staking question

Chainlink launched staking in v0.2 with the promise that it would align incentives and secure the network. Here is where it stands.

Total staked: roughly 31 million LINK. Staking ratio: 4.26% of circulating supply. The v0.2 pool has expanded to 45 million LINK capacity, but only about two-thirds is filled.

Compare this to Ethereum at 27% staked or Solana at 67%. If staking is supposed to secure the oracle network by putting validators' capital at risk, 4.26% participation says something about the incentive structure.

The current reward rate is approximately 4.75%, funded primarily by LINK emissions rather than protocol revenue. The system pays stakers with newly issued tokens, not with money earned from services. It is a circular model until fee revenue grows enough to fund rewards organically. That day has not arrived.

The oracle incident record

Chainlink is marketed as the “industry standard” for oracle security. In the last 12 months, there have been two confirmed oracle-related incidents.

In November 2025, a Chainlink oracle pricing error valued a nearly worthless wrstETH position at $5.8 million. An attacker exploited it within 30 seconds, extracting roughly $1 million from Moonwell on Base.

In May 2025, a Chainlink VWAP oracle for deUSD triggered over $500,000 in liquidations on an Euler market on Avalanche. Chainlink argued the oracle correctly reflected market activity and that it is up to individual protocols to filter the data. That is a fair technical point, but it does not change the outcome for the users who lost money.

A third incident — the MakinaFi exploit in January 2026 ($4.13 million) — involved an oracle vulnerability, though the specific attribution to Chainlink's infrastructure versus the protocol's own oracle configuration remains disputed.

Combined confirmed losses directly attributable to Chainlink oracle errors: approximately $1.5 million. This is not catastrophic relative to the $63 billion Chainlink secures. But “industry standard” carries expectations, and the track record over the past year shows the system is not infallible.

The SOC 2 Type 2 certification from Deloitte was completed in April 2026. The certification is real. But it does not retroactively erase the incidents.

The competitor nobody talks about

RedStone has roughly 40 employees. Market cap: approximately $55 million. Total value secured: $10 billion.

Their clients include BlackRock (BUIDL fund) and Apollo (ACRED). They have had zero data incidents. Their push/pull hybrid model is designed for speed without sacrificing accuracy. They integrated with 14 new lending protocols in Q1 2026 alone.

Chainlink has 400+ employees, a $7.5 billion market cap, and many of their flagship institutional clients are still “piloting.”

The capital efficiency ratio tells a story. RedStone secures $10 billion with a $55 million market cap (0.55% MC/TVS). Chainlink secures $63 billion with a $7.5 billion market cap (2.1% MC/TVS). Per dollar secured, RedStone is roughly four times more capital-efficient.

I am not saying RedStone will replace Chainlink. They probably will not. But they demonstrate that the infrastructure Chainlink provides can be built and operated at a fraction of the valuation.

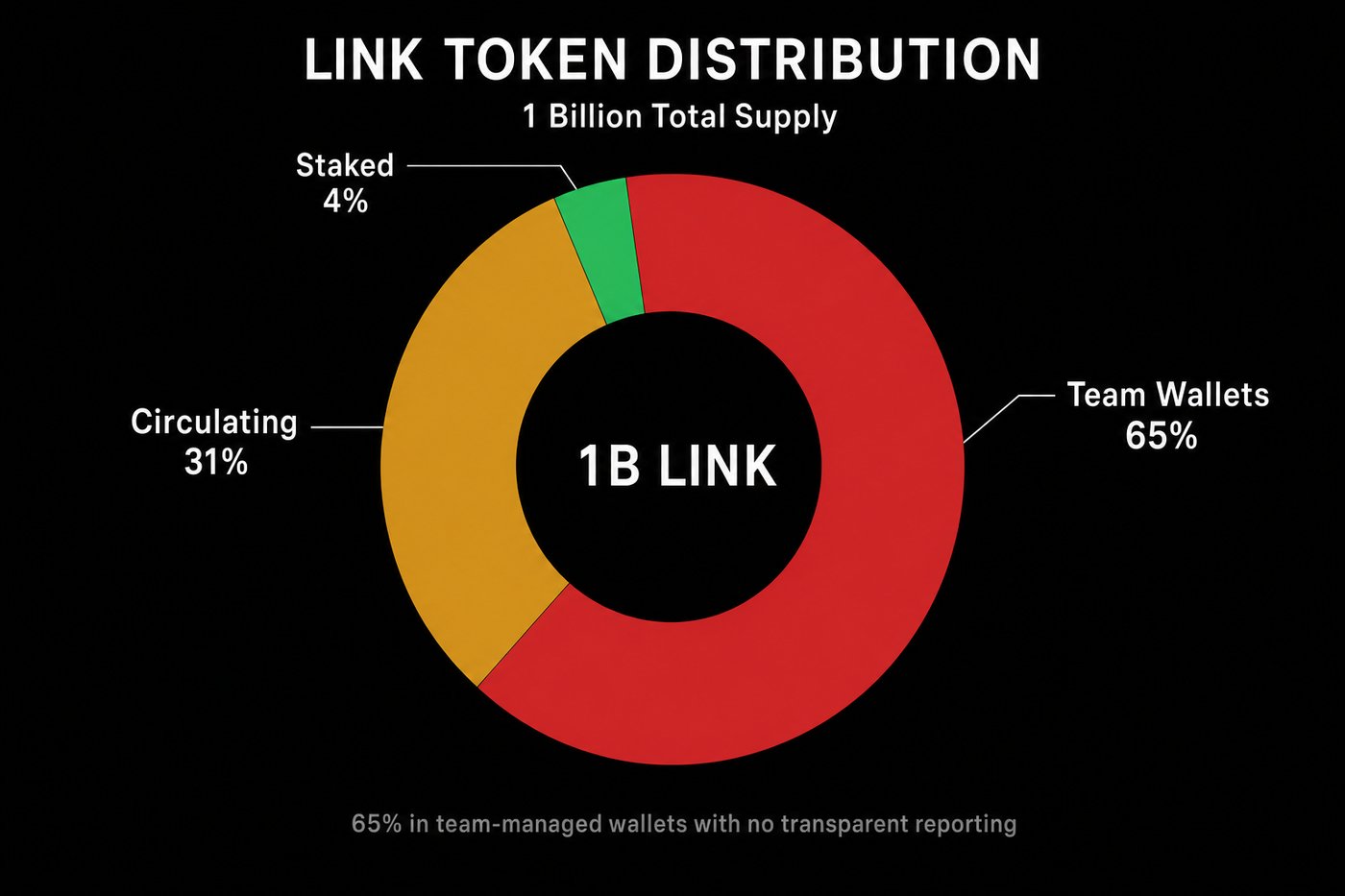

The token question

LINK has no governance rights. No fee sharing with holders. No burn mechanism. It is a payment token for oracle services, but most fees are actually paid in native gas tokens or stablecoins.

Sixty-five percent of LINK tokens are in “Team Managed Wallets.” There is no transparent treasury reporting comparable to what a public company provides. The Chainlink Reserve mechanism, which uses off-chain revenue to buy LINK, operates without public audit.

The bull case for LINK is that growing usage will eventually create demand for the token as collateral and payment. The bear case is that usage is growing but token utility is not, because the economic model does not require LINK to function. Protocols can pay in whatever token Chainlink accepts, and staking participation suggests the economic incentives are not compelling.

What this means for real-world tokenization

Here is my honest assessment.

Chainlink is important infrastructure. If you tokenize an asset, you probably need an oracle. Chainlink is the most established option. The security certifications are real. The data feeds work. The market position is dominant.

But the “Chainlink is the backbone of tokenized finance” narrative is ahead of reality by several years. SWIFT is not in production. DTCC is targeting Q4 2026. Most institutional partnerships are in pilot stages. The revenue does not match the valuation by any reasonable metric.

For tokenization practitioners like me, what matters is whether the oracle is reliable, affordable, and available for the specific asset class I am working with. For European energy storage or commercial real estate, the answer is usually simpler: the data comes from energy markets or appraisers, and the oracle layer is a commodity, not a strategic differentiator.

Chainlink may one day justify its valuation through institutional adoption at scale. The ingredients are there. But “one day” is not “today,” and the gap between the narrative and the numbers is wider than the LINK community would like to admit.

The scorecard

Technology: 8/10. CCIP security model is genuinely superior. Data feeds are battle-tested. CRE shows promise.

Revenue: 2/10. $74.5M annualized on-chain fees. 100x P/S ratio. CCIP lifetime fees: $603K total.

Institutional adoption: 5/10. Real partnerships (Amundi, DTCC) but most are pilots. SWIFT: 8 years, zero production.

Tokenomics: 3/10. No governance, no fee share, no burn. 65% in team wallets. Staking at 4.26%.

Competition: 6/10. Dominant but not irreplaceable. RedStone and Pyth demonstrate alternatives at lower cost.

RWA relevance: 7/10. Genuinely needed for tokenized assets. But the oracle is a commodity layer, not a strategic differentiator.

Overall: 5/10. Great technology. The revenue does not match the valuation.

Sources

- DefiLlama: Chainlink combined fees ($74.5M annualized), CCIP fees ($603K cumulative), oracle rankings (62% market share)

- Chainlink Q1 2026 Quarterly Review: CCIP $18B volume, 319% YoY growth

- CoinDesk: Solv migration ($700M), LayerZero exploit ($292M), DTCC integration, LayerZero admission

- Deloitte SOC 2 Type 2 report (April 2026)

- SpazioCrypto: Amundi SAFO fund ($400M in 3 weeks)

- AMBCrypto, Halborn: Moonwell exploit ($1M, November 2025)

- The Block, CryptoSlate: deUSD liquidation ($500K, May 2025)

- CoinMarketCap: LINK market cap ($7.48B), RedStone market cap (~$55M)

- StakingRewards: LINK staking ratio (4.26%), reward rate (4.75%)

- RWA.xyz: tokenized asset and protocol data

Frequently asked questions

What is Chainlink's actual revenue and how does it compare to its valuation?

Chainlink's combined on-chain fees across price feeds, CCIP, VRF, and Keepers total approximately $74.5 million annualized according to DefiLlama. With a market cap of $7.5 billion, that is a price-to-sales ratio of roughly 100x for a data relay service. Off-chain enterprise revenue is claimed but the Chainlink Reserve mechanism that converts it into LINK is not publicly auditable.

How much revenue has CCIP actually generated?

CCIP processed approximately $18 billion in cross-chain transfer volume in Q1 2026 alone, with 78% quarter-over-quarter growth and 319% year-over-year growth. However, cumulative CCIP fees over the entire lifetime of the protocol total roughly $603,000. That is an effective take rate of 0.003%, or three thousandths of one percent.

Why is the Chainlink and SWIFT partnership still not generating revenue after 8 years?

Chainlink and SWIFT have announced proof-of-concepts, phase 1 and phase 2 pilots, and integration milestones every year since 2018. As of May 2026, the production revenue flowing through Chainlink from SWIFT is zero. Twenty-four financial institutions are described as “participants” in various pilots, but none has committed to a binding production timeline. The relationships are real; the revenue is not.

Did Chainlink win the LayerZero migration through product quality?

Partly. In April 2026, the Lazarus Group exploited KelpDAO through a single-verifier configuration on LayerZero, stealing about $292 million in rsETH. Over the following weeks, more than $1.2 billion in protocol value migrated to Chainlink CCIP, including Solv Protocol ($700M) and Re Protocol ($475M). Chainlink's multi-validator security model prevents this exact attack, so the win is partly product-driven. But the trigger was a competitor's catastrophic failure, not Chainlink innovation or marketing.

Is Chainlink staking secure and well-incentivized?

About 31 million LINK is staked, representing 4.26% of circulating supply. The v0.2 pool can hold 45 million LINK but only two-thirds is filled. By comparison Ethereum is around 27% staked and Solana about 67%. The current 4.75% reward rate is funded primarily by LINK emissions, not protocol revenue, which makes the incentive circular until fee revenue grows enough to fund rewards organically.

Are Chainlink oracles actually reliable for real-world asset tokenization?

Reliability is high relative to the $63 billion Chainlink secures, but it is not zero. In the past 12 months there have been two confirmed Chainlink oracle pricing incidents: a wrstETH error in November 2025 on Moonwell that cost users about $1 million, and a deUSD VWAP issue in May 2025 on Euler/Avalanche that triggered over $500,000 in liquidations. Deloitte completed a SOC 2 Type 2 audit in April 2026, which is real institutional-grade certification, but it does not retroactively erase the incidents.

How does RedStone compare to Chainlink on capital efficiency?

RedStone has roughly 40 employees and a $55 million market cap, and secures $10 billion in assets including BlackRock's BUIDL fund and Apollo's ACRED. Chainlink has 400+ employees, a $7.5 billion market cap, and secures $63 billion. Per dollar secured, RedStone's market-cap-to-total-value-secured ratio is 0.55% versus Chainlink at 2.1%, making RedStone roughly four times more capital-efficient on that metric.

Should I buy LINK as an investment in tokenization?

Nothing in this article is investment advice. LINK has no governance rights, no fee sharing with holders, and no burn mechanism. Most fees are paid in native gas tokens or stablecoins, not in LINK. 65% of LINK supply sits in “Team Managed Wallets” with no comparable public reporting to a public company. The bull case is that scaling usage eventually requires LINK as collateral or payment; the bear case is that usage can grow without that requirement and the staking participation rate of 4.26% suggests the incentives are not currently compelling. Make your own decision based on the data, not the narrative.

This is the sixth in a series where I take a real project and run the same due diligence I would use before putting my own money in. To get the next one first, join the Telegram or follow me on LinkedIn.

Nothing in this article is investment advice. I do not hold LINK tokens. I have no financial relationship with Chainlink Labs, RedStone, Pyth Network, LayerZero, or any of the issuers named. Data points are sourced from publicly available services (DefiLlama, RWA.xyz, CoinGecko, StakingRewards) and were accurate as of May 12-13, 2026. Numbers update over time. Do your own research.