Reental has been tokenizing real estate since 2020. Five years. Over a hundred projects. Properties in Spain, Argentina, the Dominican Republic, Dubai, and soon Miami. They tokenized an apartment on the 63rd floor of the Burj Khalifa. They have an NBA veteran on their advisory board. $71 million in distributed asset value on rwa.xyz.

Real buildings. Real tenants. Real exits. Also, real contradictions in their own data, a legal structure most investors have never read, and a utility token trading $14,500 a day on a $30 million market cap.

What Reental Actually Does

Reental turns real estate into tokens on the Polygon blockchain. You buy a token for around $100, the platform uses the pooled capital to acquire a property, manages the rental, and pays you monthly returns in USDT. When the property is sold or refinanced, you get your capital back plus any appreciation.

You buy a token for $100 and own a fraction of an apartment somewhere in Valencia or Dubai. The platform finds tenants, collects rent, handles plumbing. You check your wallet once a month.

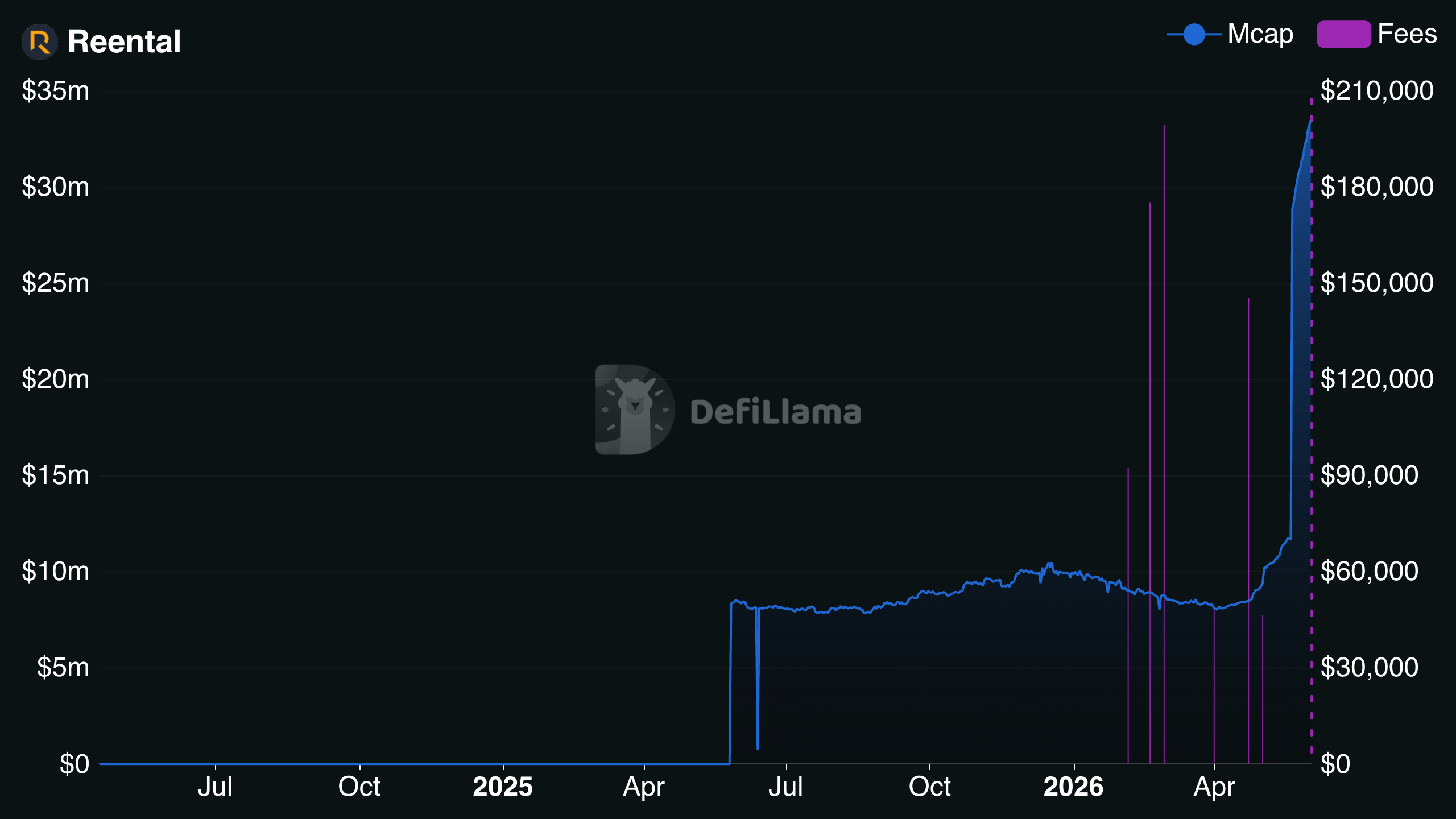

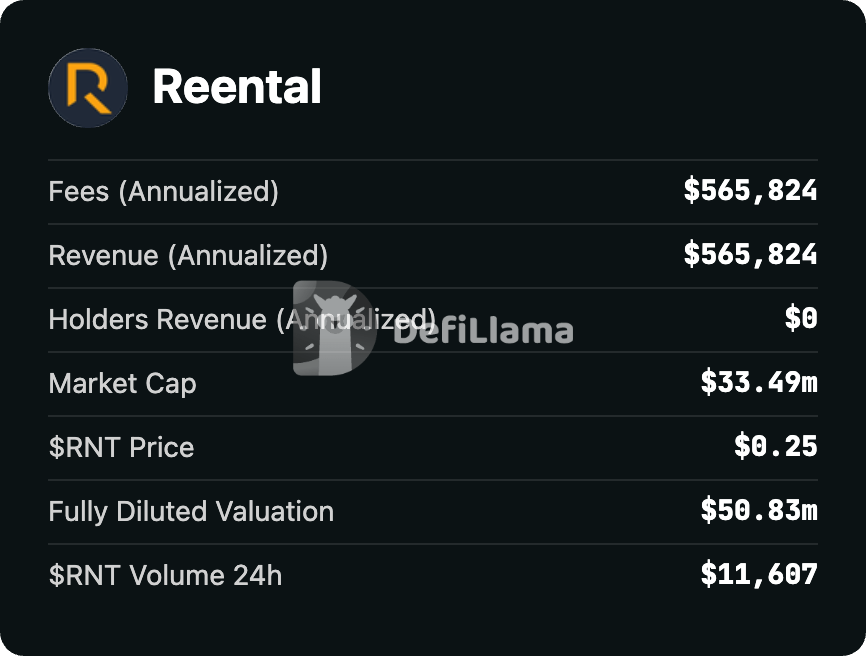

They have 45 active assets tracked on rwa.xyz, with a distributed asset value of $71.6 million and 10,982 on-chain holders. Properties range from student housing in Valencia to developments in Atlanta and Houston to luxury apartments in Dubai's Burj Khalifa. DefiLlama tracks their annualized protocol fees at roughly $566,000. Q1 2026 brought in $467,000; Q2 so far, $240,000. And here is the detail most people miss: Token Holder Net Income on DefiLlama reads $0. RNT holders receive nothing from protocol revenue. The fees go to the company.

That part is simple. What happens when you read the actual legal documents is not.

The Team

Eric Sanchez Galvez, the CEO, has an unusual background. Professional basketball player for 15 years. Then computer engineering. Then co-founded Chekin, a tourism tech company that went through 500 Startups, in 2017. Founded Reental in 2020. Not a typical real estate resume, but the tech founder angle is relevant for a platform that is fundamentally a software product wrapped around buildings.

Fernando Ors, the chairman, brings the finance credibility. Dual US/Spain citizen. MBA from IESE. Executive programs at Harvard, Stanford, MIT, and Berkeley. Led IPOs including a unicorn valuation. 20+ years as a strategy consultant and venture capitalist.

The advisory board includes Luis Scola, the Argentine basketball legend who played 14 NBA seasons and won Olympic gold. Also Jon Fatelevich (Top 100 Business Angel in Spain) and Gustavo Rossi (founder of Alquiler Seguro, one of Spain's largest rental guarantee companies).

The team is real. 53 employees across marketing, tech, finance, legal, and real estate. Five years of operation. Nobody disappeared with the money. In tokenized real estate, that sentence alone puts you ahead of most competitors.

The Numbers: What They Say vs. What Exists

Reental's homepage says 41,315 registered users. Another section of the same website says 32,200. rwa.xyz, which tracks on-chain data, shows 10,982 holders. Of those, only about 550 to 565 addresses are active monthly. That is roughly 5% of holders doing anything in a given month. The gap between "registered users" and "on-chain holders" makes sense. The gap between two numbers on the same website does not. And the gap between 10,982 holders and 550 active ones is the number nobody puts on the homepage.

They claim 108 tokenized projects. On another page, 116. rwa.xyz tracks 45 active assets. The difference is explained by completed projects that no longer appear on tracking platforms. But when you market "100+ projects" without specifying how many are active versus closed, you are managing perception, not reporting data.

Total tokenized value: Reental says "100 million plus." rwa.xyz shows $71.6 million in distributed asset value. Again, the gap is partially explained by returned capital from closed projects. But the headline number and the verifiable number are not the same, and nobody puts an asterisk next to "100M+" on the homepage.

Their stated average return on closed projects is 15.39%. On another page, 16.52%. The specific success stories they highlight tell a different story entirely: Sagunto 2 at 34.37%, Valencia 2 at 32.99%, Sevilla 3 at 31.49%. If your best projects returned 27 to 34 percent and your average is 15 to 16 percent, there are underperformers pulling that number down significantly. Those projects are not on the success stories page.

One more detail for Spanish investors: Reental applies a 19% withholding tax on returns automatically. On a 15% gross yield, that brings your net down to roughly 12% before any platform fees. Nobody leads with that number.

None of this means the platform is fraudulent. It means the data presentation is optimized for marketing, not for due diligence. And when you are asking people to invest $100 at a time into security tokens with limited liquidity, the difference matters.

The Legal Structure Nobody Reads

In Spain, Reental does not sell you a piece of a building. They sell you a participatory loan. Your token represents a credit right against Reental Token SL, the issuing subsidiary. You are lending money to a company that operates a property. Your return is linked to the property's performance, but your legal position is that of a lender, not an owner.

In the United States, the structure is different. Each property is wrapped in an LLC, and your token represents a share of that LLC. This is closer to actual fractional ownership.

The Spanish structure has a specific risk that most retail investors will not discover until it is too late. Under Spanish insolvency law, participatory loans rank below ordinary debt. If Reental Token SL goes bankrupt, the secured creditors get paid first. Then the ordinary creditors. Then, if anything is left, the holders of participatory loans. You are last in line.

Reental operates under Spain's Law 6/2023 on Securities Markets, which allows DLT-represented securities. They are not operating in a regulatory vacuum. But being compliant and being safe for investors are two different conversations.

For US investors: Reental operates under SEC Regulation D 506(c) for accredited investors and Reg S for non-US persons. A Form D was filed on EDGAR on July 19, 2024 under CIK 0002007865 (Reental Holding Co). The filing confirms the Reg D exemption but provides minimal financial detail. A Form D is a notice, not an audit. It tells the SEC the offering exists. It does not tell investors how the money is being managed.

The RNT Token Problem

Reental has two types of tokens. The property STOs (security tokens representing specific real estate investments) and RNT, a utility token that powers their ecosystem.

RNT trades on SushiSwap on Polygon. Current price: approximately $0.23. Market cap: around $30.7 million. Liquidity in the pool: about $1.95 million.

The 24-hour trading volume: $14,500.

That is not $11,600 thousand. That is eleven thousand six hundred dollars in daily trading volume for a token with a thirty-three million dollar market cap. 0.03% daily turnover. If you held $50,000 in RNT and tried to sell, you would move the price. The largest single wallet holds 26.8% of the total supply. If that wallet exits, the price collapses. There is no depth to absorb it.

The RNT contract is a proxy contract, meaning it is upgradeable. The admin can change the logic. For a token marketed as part of a decentralized ecosystem, that is a centralization risk worth noting.

RNT provides "enhanced returns" and "early access to projects" for holders. But Token Holder Net Income on DefiLlama reads $0. The protocol makes money. RNT holders do not share in it. Some investors get better deals because they hold a speculative utility token, not because they are better at evaluating real estate. The platform is tying investment access to a token you cannot meaningfully sell and that pays you nothing. That should bother people more than it does.

The Liquidity Reality

The secondary market for Reental property tokens is peer-to-peer. There is no central order book, no automated market maker, no Uniswap pool for individual property tokens. If you want to sell before the property exits, you need to find a buyer on external P2P platforms.

RealT built its own YAM marketplace for secondary trades. Lofty has a built-in market. Reental's approach is closer to "figure it out yourself."

Monthly transfer volume across all Reental assets on rwa.xyz: $5.36 million. That number dropped 61.78% in the past 30 days. Volume is going the wrong direction.

Reental has introduced Reenlever, a DeFi lending protocol integrated with AAVE that lets you borrow against your property tokens. The idea is smart. But it adds leverage to an already illiquid asset class. If property token values drop while you have a loan against them, you face liquidation on an asset you cannot quickly sell. That is a risk worth understanding before you click "deposit."

What Reental Gets Right

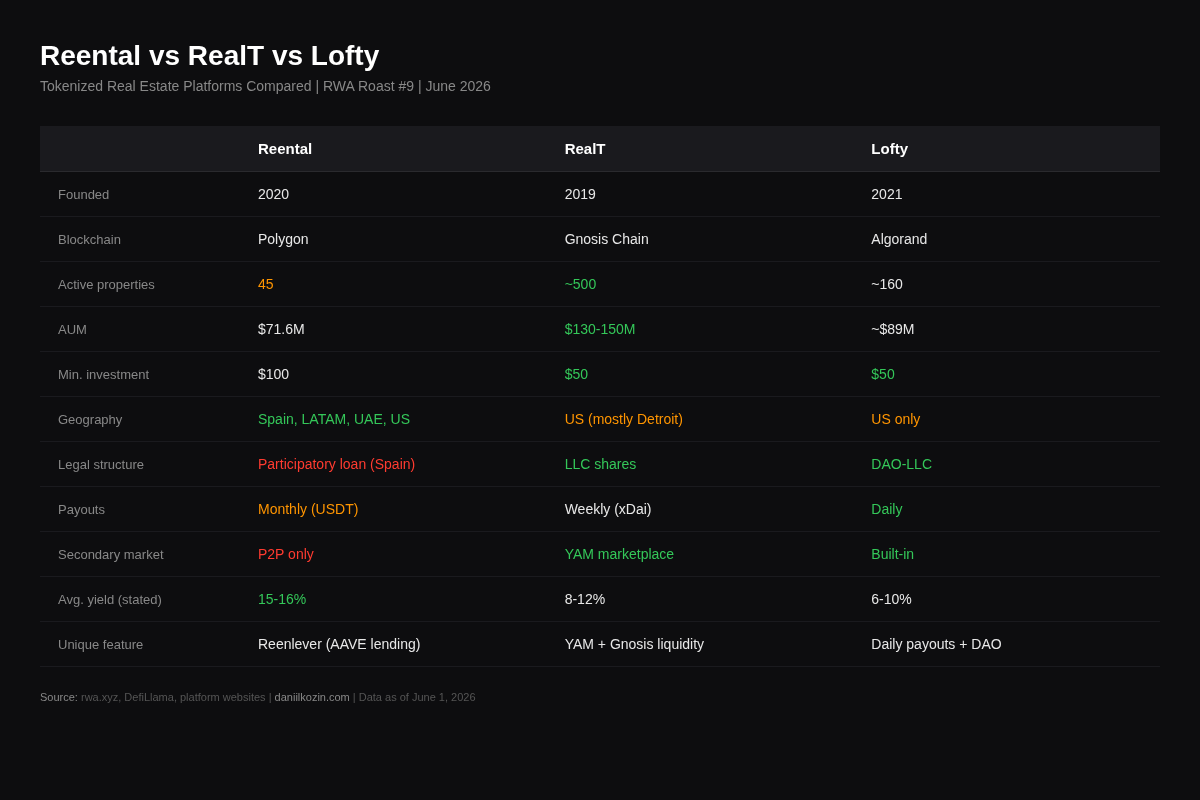

Most tokenized real estate platforms are stuck in one country. RealT is almost entirely US, mostly Detroit. Lofty is US only. Reental operates across Spain, Argentina, Mexico, the Dominican Republic, the UAE, and is expanding into the US. If you want European and Latin American rental exposure through a single crypto-native platform, there are not many alternatives.

The closed project returns, even at the stated average of 15 to 16 percent, are competitive for the space. The question is what the underperforming projects looked like, but the average itself is credible for value-add rental strategies in southern Europe and Latin America.

The Burj Khalifa tokenization, $1.25 million funded in 10 days for a 63rd-floor apartment, builds brand credibility even if the yield is not the highest. The community put real money behind a prestige asset. That says something about trust.

And five years of operation with completed exits, capital returned, and consistent payouts is a track record most RWA projects cannot show. Properties were bought. Tenants paid rent. Buildings were sold. In a space where most competitors are still "coming soon," that matters.

How Reental Compares

| Reental | RealT | Lofty | |

|---|---|---|---|

| Founded | 2020 | 2019 | 2021 |

| Blockchain | Polygon | Gnosis Chain | Algorand |

| Active properties | 45 (rwa.xyz) | ~500 | ~160 |

| AUM | ~$71.6M | $130-150M | ~$89M |

| Min. investment | ~$100 | ~$50 | ~$50 |

| Geographic focus | Spain, LATAM, UAE, US | US (Detroit, others) | US rental homes |

| Legal structure | Participatory loan (Spain) / LLC (US) | LLC shares | DAO-LLC |

| Payouts | Monthly (USDT) | Weekly (xDai) | Daily |

| Secondary market | P2P (limited) | YAM marketplace | Built-in marketplace |

All three have real properties generating real rent. Reental wins on geographic spread. RealT wins on scale and secondary trading. Lofty wins on payout speed and built-in exit. The tradeoff depends on what you value more: international exposure or the ability to sell tomorrow.

The Scorecard

| Category | Score | Notes |

|---|---|---|

| Asset Quality | 7/10 | Real properties, geographic diversification, prestige projects (Burj Khalifa). Rental income verified through monthly USDT payouts. |

| Token Structure | 4/10 | Participatory loan in Spain ranks below ordinary debt in insolvency. US LLC structure is stronger but only applies to US offerings. RNT is upgradeable proxy contract with 26.8% whale concentration. Dual structure creates confusion. |

| Team | 7/10 | Five-year track record. Finance credibility (Fernando Ors). 53 employees. NBA advisory. CEO background is tech, not real estate, but platform is fundamentally a tech product. |

| Yield / Returns | 6.5/10 | Advertised 10-19%. Average closed at 15-16%. Some projects hit 27-34%. Monthly payouts are real. But success stories appear cherry-picked and no independent audit of returns found. |

| Transparency | 4/10 | Three different user counts on one website. Two different project counts. Two different average return figures. AUM claims exceed verifiable data. No Form D found on EDGAR for primary issuer. |

| Liquidity | 3/10 | P2P secondary market only. No central order book. RNT daily volume ~$14,500. Monthly volume dropped 62%. 26.8% of RNT in one wallet. Reenlever adds leverage risk to illiquid assets. |

| Innovation | 7/10 | Multi-country real estate tokenization is rare. Reenlever (AAVE-integrated DeFi lending on property tokens) is novel in the space. Burj Khalifa project shows ambition. |

| Regulatory | 5.5/10 | Form D filed July 2024 (CIK 0002007865). Operates under Spanish Law 6/2023. KYC/AML in place. No enforcement actions found. Dual-jurisdiction complexity adds risk. |

| Overall | 5.3/10 | Five-year track record meets a participatory loan structure. Real properties meet inconsistent data presentation. The platform is legitimate; the structural details deserve scrutiny. |

The Same Four Questions

I ask these in every RWA Roast. They cut through the noise.

1. Does the yield survive real math?

Conditional pass. The 15-16% average on closed projects is plausible for value-add rental strategies in Spain and Latin America. But the spread between the "average" (15-16%) and the success stories (27-34%) suggests significant variance. Without seeing the full distribution including underperformers, it is impossible to evaluate risk-adjusted returns. Monthly USDT payouts are verifiable on-chain, which is a plus. Conditional pass.

2. What do you actually own?

Fail in Spain. Conditional pass in the US. In Spain, you own a participatory loan that ranks below ordinary creditors in insolvency. You do not own the building or a share of an entity that owns the building. You hold a contractual claim against a subsidiary. In the US, the LLC structure provides actual fractional ownership. Most Reental investors are in the Spanish structure. Spanish offering: Fail. US offering: Pass.

3. Can you actually exit?

Partial fail. The secondary market is P2P with no central mechanism. Reenlever provides a DeFi workaround (borrow against tokens) but that is leverage, not liquidity. Property tokens are effectively locked until the platform decides to exit the property. Your exit timeline depends entirely on Reental's business decisions. Partial fail.

4. Skin in the game?

Conditional pass. Reental claims "we invest our money in every project" but does not disclose the percentage or terms of co-investment. The team has been operating for five years and has not disappeared, which is behavioral evidence of alignment. But "we invest alongside you" without a specific percentage is a marketing claim, not a commitment. Conditional pass.

The Bottom Line

Reental is a real platform with real buildings, real tenants, and a five-year track record that most RWA projects would envy. The geographic diversification alone makes it interesting. The team has legitimate credentials. Properties have been bought, rented, and sold at a profit.

But the participatory loan structure in Spain means most investors do not own what they think they own. They hold an unsecured credit right that ranks last in line if anything goes wrong. The inconsistent numbers across Reental's own website raise questions about data discipline. And the RNT token, with its $14,500 daily volume, is a utility layer built on a liquidity desert.

The question for an investor is specific: can you accept a participatory loan structure, limited secondary market liquidity, and unaudited return claims in exchange for exposure to diversified international real estate through a five-year-old platform with completed exits?

If yes, read the loan agreement first. Not the marketing page. The agreement.

Frequently Asked Questions

Is Reental a good investment?

Reental has a five-year track record, real properties, and completed exits returning 15-34%. However, most investors hold participatory loans, not equity. Returns are unaudited, the secondary market is limited, and the RNT utility token has minimal liquidity. It is a legitimate platform with real limitations.

What does a Reental token actually represent?

In Spain, it represents a participatory loan (a credit right against a Reental subsidiary). In the US, it represents shares in an LLC that owns the property. The Spanish structure is weaker because participatory loans rank below ordinary debt in insolvency.

Reental vs RealT: which is better?

RealT has more properties (~500 vs 45 active), a built-in secondary market (YAM), and weekly payouts. Reental offers geographic diversification (Spain, LATAM, UAE) and higher advertised yields (15-16% average vs RealT's 8-12%). RealT's LLC structure is legally stronger than Reental's participatory loan in Spain.

Reental vs Lofty: which is better?

Lofty offers daily payouts, a built-in secondary market, and a lower minimum ($50 vs $100). Reental offers international exposure beyond the US market and higher yields. Lofty's DAO-LLC structure provides governance rights that Reental's participatory loan does not.

Is Reental regulated?

Reental operates under Spain's Law 6/2023 for DLT securities. A Form D was filed with the SEC on July 19, 2024 (CIK 0002007865) confirming Reg D 506(c) compliance for US investors. No regulatory enforcement actions found.

Can you sell Reental tokens before the property exits?

Only through P2P platforms. There is no central secondary market or order book. Reenlever allows borrowing against tokens via AAVE integration, but that is leverage, not a sale mechanism.

What is the RNT token?

RNT is Reental's utility token (separate from property tokens). It provides early access to projects and enhanced returns. Current daily trading volume is approximately $14,500, which represents extremely thin liquidity for a token with a ~$30M market cap.

How does Reental make money?

Reental charges an 8% management fee on property operations plus upfront offering fees on each property launch. DefiLlama tracks annualized protocol revenue at roughly $566,000 (Q1 2026: $467K, Q2 2026: $240K). Token Holder Net Income is $0. RNT holders do not share in protocol revenue.

What about taxes for Spanish investors?

Reental applies a 19% withholding tax automatically on returns for Spanish residents. On a stated 15% gross yield, net after withholding is closer to 12% before platform fees.

Daniil Kozin structures tokenized real-asset deals in Europe and writes the RWA Roast series to cut through the conference slides. Previous roasts: GromaCoin, Centrifuge, Chainlink, Figure, Stellar, Kelp DAO, Syrup, Ondo, Canton. Full archive at daniilkozin.com/blog.

Disclaimer: I do not hold RNT tokens or any Reental property tokens. This is not investment advice. Do your own research.

Sources:

- Reental Homepage

- Reental FAQ

- Reental Team Page

- Reental Success Stories

- Reental on rwa.xyz

- Reental on Republic (Reg CF)

- RNT on CoinGecko

- RNT on DEX Screener

- Reental Trustpilot Reviews

- Reental Burj Khalifa Launch

- Reenlever Blog Post

- Luis Scola Joins Reental

- TokenizedLiving Reental Review

- LMRE Interview with Eric Sanchez

- Refresh Miami - Reental Expansion

- CrowdSpace - Reental

- SEC EDGAR

- CoinGecko 2025 Annual Crypto Report

Data as of June 1, 2026. RWA space moves fast. Always verify live metrics and do your own due diligence on tokenized real estate offerings.