Seth Priebatsch dropped out of Princeton, built a mobile payments company for restaurants called LevelUp, raised roughly $108 million in total funding over 11 years, and sold it to Grubhub for $390 million in cash. He became Grubhub's Chief Revenue Officer. Then he decided to tokenize apartment buildings in Boston.

I spent a week going through the Groma Real Estate Trust structure, the crowdfunding filings, the whitepaper, the on-chain data, and the AI claims. What I found is a project with real buildings, real revenue, and a founder who clearly knows how to raise money. But also a project with 218 token holders, no secondary market, a roughly 3% dividend yield that nobody has independently confirmed, and an AI operating system that nobody outside the company has tested.

What Groma Actually Does

Groma buys, renovates, and operates small apartment buildings. Two to twenty units each. What the industry calls "micro-multifamily." They focus on Greater Boston, with plans to expand to Brooklyn, Chicago, Los Angeles, and Austin.

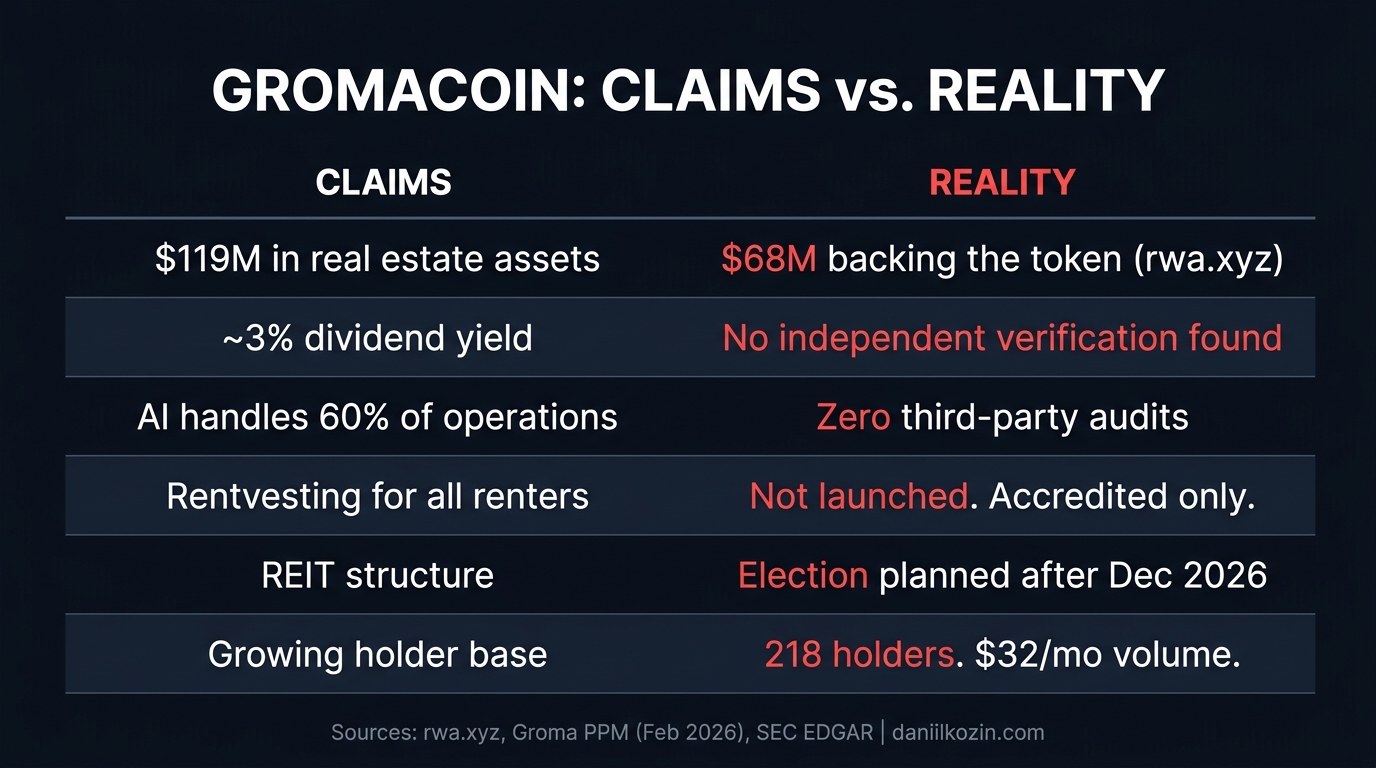

The portfolio today is over 125 buildings, roughly 700 units across the tokenized Trust, with a total asset value that depends on who you ask. rwa.xyz says $68 million. Groma says $119 million. More on that gap later.

Revenue is around $2 million with growth claims of 25% year-over-year. Groma says they have paid quarterly cash distributions consistently since 2024, though I could only verify five consecutive quarters from their Republic filings as of late 2023. The "10 consecutive quarters" claim that appears on their site is plausible given the timeline, but not independently confirmed.

The structure is interesting. Groma is set up as an open-ended private REIT. The Groma Real Estate Trust. Token holders own shares in that trust. Each GromaCoin equals one share. The token runs on Base, uses the ERC-3643 compliance standard, and sits at roughly $1.04 per share.

They also have a concept called "rentvesting." If you rent a Groma apartment, you can turn a portion of your rent into ownership in the Trust. You pay rent and build equity at the same time. It is a clever idea that aligns the interests of tenants and investors in a way most REITs do not even attempt. However, as of May 2026, rentvesting has not actually launched for non-accredited renters. It is described as "soon-to-launch" in their March 2026 partnership announcement with Modern Treasury. So for now it remains a concept, not a product.

The Founder: From Grubhub to Real Estate

Priebatsch's background is worth understanding because it explains both the strengths and the questions around this project.

He won the Princeton Business Plan Competition, dropped out, and founded LevelUp at 21. LevelUp built mobile payment systems for restaurants. Over 11 years he raised approximately $85 million in venture capital (some sources cite $108 million in total lifetime funding including all rounds) and grew the company until Grubhub acquired it for $390 million in cash in July 2018. At Grubhub he ran revenue operations as CRO.

His co-founder at Groma is Chris Lehman. Harvard degree in Social Studies (class of 2013). Career path: consulting, web development at General Assembly, tech analyst at Wayfair. No prior real estate or financial services background before joining Groma around 2020.

Priebatsch has invested over $5 million of his own money into the Groma Real Estate Trust, and reportedly over $5 million into GromaCorp as well. That is meaningful skin in the game. He clearly knows how to build and sell companies.

The question is whether building restaurant payment apps is relevant experience for operating 700 apartment units across 125 buildings. Priebatsch would probably argue that the operational complexity is similar and that tech-enabled management is his edge. Skeptics would argue that real estate has risks that no amount of software experience prepares you for.

Both arguments have merit.

The Numbers: What rwa.xyz Shows vs. What Groma Claims

This is where it gets confusing, and the confusion itself is a problem.

rwa.xyz lists GromaCoin at $68.2 million in total asset value. Groma's own materials and press releases say $119 million. Their February 2026 PPM (private placement memorandum) says the Trust raised $58.8 million from over 100 shareholders as of November 2025.

Three different numbers for what sounds like the same thing. Here is what I believe is happening:

The $119 million includes all Groma-affiliated vehicles. That means Fund I (a closed-end partnership with 39 buildings), the GromaREIT on Republic (47 buildings, roughly $31 million AUM), and the Groma Real Estate Trust itself (the tokenized vehicle with 125+ buildings). These are not the same entity. The $68 million on rwa.xyz reflects only the tokenized Trust assets backing the GRO token. The $58.8 million in the PPM is the equity raised in that Trust as of late 2025.

For an investor trying to understand what they actually own when they buy GromaCoin, this matters. You own a share in the Groma Real Estate Trust. Not in Fund I. Not in GromaREIT on Republic. The Trust.

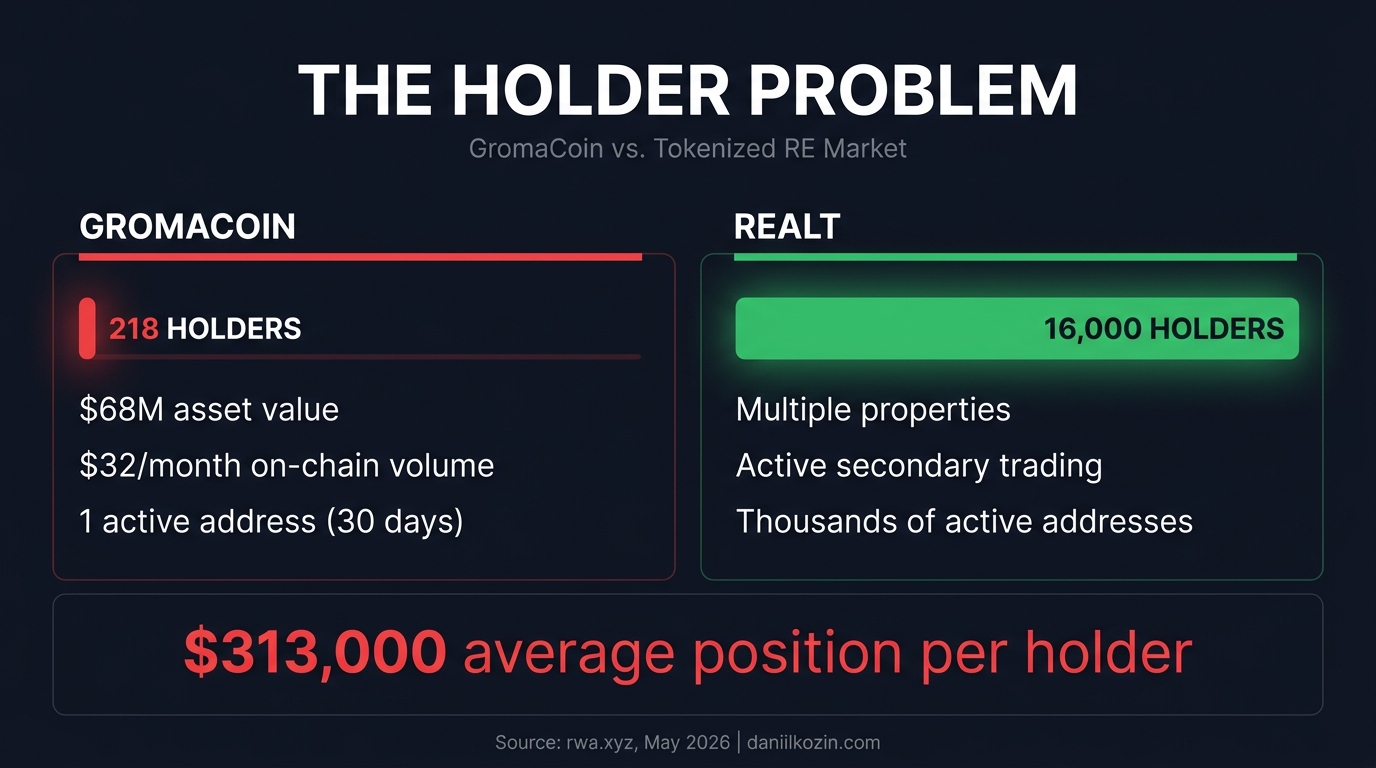

Holders: 218 as of late May 2026. Up roughly 15% in the last 30 days. For a $68 million asset, 218 holders implies an average position of around $313,000 per holder. That number is almost certainly skewed by a few large institutional investors and Priebatsch's own stake.

The on-chain reality is even more telling. Monthly transfer volume on Base: $32. Not $32 thousand. Not $32 million. Thirty-two dollars. Active addresses in the last 30 days: 1. Monthly transfers: 31. This token is not illiquid. It is not trading at all. It exists as a static ledger entry.

The Yield Question

Groma's materials suggest approximately 3.3% current dividend yield, paid quarterly, with a target of 4-5% for 2026. Including estimated asset appreciation of around 4-8%, the all-in return target is 7-11%.

I could not find this yield figure confirmed in any independent source. The PPM mentions "durable current income" as an objective but does not specify a percentage. Their Republic page (from 2024) mentions Fund I properties generating approximately 6% yield and $80,934 in distributions across 5 quarters. The Thesis Driven analysis says Fund I delivered roughly 20% IRR and 4% average annual distributions.

The problem is that Fund I is a different vehicle than the open-ended Trust. The yield from a closed-end 2020-era acquisition fund in Boston is not necessarily what the 2025-2026 open-ended REIT delivers.

For context: Boston multifamily cap rates in 2026 are 4.5-5.5% for stabilized properties. The average public REIT dividend yield in the US is around 4-5%. RealT, one of the largest tokenized real estate platforms, offers 8-12% rental yield. Lofty pays 5-8%.

If Groma's yield is truly around 3%, that is below all of these. The all-in 7-11% (including appreciation) would be competitive, but only if the appreciation materializes year after year.

One thing the original version of this article missed: Groma charges a 1% annual management fee and a 12.5% performance fee after certain return hurdles. On a 7-8% gross return, the performance fee alone could reduce net returns by close to a percentage point.

The Holder Problem

218 holders for $68 million is the single most important number in this analysis.

RealT, which also tokenizes residential real estate, has roughly 16,000 holders across its portfolio. Groma has 218. The difference is not incremental. It is structural.

With 218 holders, no functioning secondary market, and $32 in monthly on-chain volume, GromaCoin is effectively frozen. You can redeem tokens directly from the Trust at current coin value, but the process has period limits, blackout windows around NAV calculations, and is subject to the Trust's cash position. If multiple holders want to exit at the same time, the Trust may not have the liquidity to service those redemptions without selling properties.

This is not a theoretical risk. It is the central risk of the entire structure.

Groma says they are working with partners on secondary liquidity. There is a concrete development here: in Q2 2026, Birch Hill is deploying an initial Morpho lending market on Base with GromaCoin as collateral and USDC lending, with Yearn curating the vault. This would let holders borrow against their tokens without selling.

That is a real and interesting DeFi integration. But it also introduces new risks. Oracle failures. Smart contract bugs. Liquidation cascades on an illiquid asset. And the fundamental circularity of borrowing against something nobody can sell.

As of today, there is still no exchange, no AMM, no order book, and no market maker for GRO tokens. You buy in. You hope you can get out.

The Fundraising: Three Vehicles, Two Platforms

Groma is raising money across multiple structures, and this complexity is something retail investors need to understand.

Fund I (closed): A closed-end partnership from 2020-2021. 39 buildings, 136 units. $62.5 million acquisition cost, $82.3 million valuation as of Q4 2024. This is finished and separate from the token.

GromaREIT on Republic: Raised approximately $16 million in equity. 47 buildings, 305 units. Class A Common Stock. This is a separate entity from the tokenized Trust.

Groma Real Estate Trust (the token): The open-ended private REIT. On Wefunder (Reg CF, minimum $100, $5 million maximum raise, $57.34 million valuation) and as GromaCoin on Base. 125+ properties, 600+ units. This is what GRO token holders own.

The dual-platform crowdfunding approach is not illegal. Many companies do it. But the multi-vehicle structure means a retail investor needs to understand exactly which entity holds which properties and what their specific claims are.

Institutional capital is real: $95 million from institutions and family offices in 2025 alone, up from $43 million in 2024. Backers include Bantam Group, Beacon Venture Partners, Castle Island Ventures, Echelon Capital, and L1D.

I searched SEC EDGAR for a Reg A+ filing (Form 1-A). Found nothing. The PPM (February 2026) does not mention Reg A+ specifically. It says the Trust "may become a public reporting company" if it exceeds certain thresholds, and that it plans to elect REIT status after the calendar year ending December 31, 2026.

That last part is worth emphasizing. The REIT election has not happened yet. If Groma fails to qualify, distributions would be taxed at the corporate level and then again at the investor level. The entire tax structure of the investment changes. The article's claim about "Reg A+ in H1 2026" could not be verified from any public source.

Also worth noting: GromaCoin is currently restricted to accredited investors under Reg D Rule 506(c). The "democratization of real estate" narrative is still largely theoretical until either Reg A+ happens or the non-accredited investor program launches.

The AI: Grobot

Groma claims that an AI system called Grobot handles 60% of recurring operational tasks across their portfolio. Scheduling maintenance, reconciling invoices, fielding resident requests, tracking energy and water data, producing task orders for maintenance technicians.

In Q4 2025, according to their materials, Grobot modeled 1,100+ properties and filtered 90-95% before full underwriting, saving an estimated 1,700 analyst hours. They claim operating expense ratios reduced from 40-45% to 30-35% within 24 months of acquisition. NOI uplift of roughly 35% within two years.

The concept makes sense. Small multifamily buildings are operationally messy. Dozens of vendors, thousands of service requests, utility bills, lease renewals. If you can automate even a portion of that, you reduce costs and scale faster.

But I could not find a single independent verification of any of these numbers. No third-party audit. No benchmark against comparable property management operations. No before-and-after data published externally. The PPM includes a disclaimer that Grobot "outputs depend on quality of data and require human oversight."

Priebatsch is a tech founder. Building internal tools is what he does. I do not doubt that Grobot exists or that it handles some operational tasks. But "60% automation" is a marketing claim until someone outside Groma confirms it. And without knowing what "recurring operational tasks" means as a denominator, the number is meaningless. Sixty percent of what?

The Verdict

Here is what Groma gets right.

The assets are real. Over 125 buildings, 700+ units, real tenants paying real rent. The founder has a track record of building and exiting a company at scale. He put $5 million of his own money in. The team is growing. Revenue is growing. Institutional investors committed $95 million in 2025. The rentvesting concept is genuinely innovative if it ever launches. The Morpho DeFi integration is ahead of any other tokenized real estate project.

Here is what concerns me.

218 holders and no secondary market means zero liquidity for anyone holding this token today. The on-chain volume is $32 per month, which means the token is functionally inert. The dividend yield is approximately 3% before a 12.5% performance fee, which lands below both traditional REITs and tokenized competitors. The Reg A+ filing that would enable broad retail participation has not been filed and cannot be verified. The REIT election has not happened yet. The AI claims are unverified by anyone outside the company. The founder's background is restaurant payments, not real estate. The valuation numbers differ significantly depending on which source and which vehicle you look at. And the "rentvesting" product that makes the thesis so compelling has not launched for non-accredited participants.

Groma is one of the more serious projects in tokenized real estate. The buildings exist. The revenue exists. The team is competent. But "more serious than most" is a low bar in an industry where the entire global tokenized real estate market is roughly $300 million.

The question for an investor is straightforward. Can you accept approximately 3% dividends, zero secondary liquidity, 218 co-investors, unverified AI claims, a pending REIT election, and an accredited-investor-only restriction, for a real estate portfolio managed by a team whose primary experience before this was restaurant technology?

If the answer is yes and you believe in the long-term thesis, Groma might be one of the better options in a very thin market. If the answer is no, there are traditional REITs with higher yields, deeper liquidity, and decades of operating history available to you right now.

Scoring (out of 10)

| Category | Score | Notes |

|---|---|---|

| Asset Quality | 7/10 | Real buildings, real revenue, real tenants. Boston market is stable. Verified. |

| Token Structure | 4/10 | ERC-3643 compliance is good. But 218 holders, $32 monthly volume, no secondary market. Token is functionally inert. |

| Team | 6/10 | Strong founder with verified $390M exit. Co-founder has no RE background. |

| Yield / Returns | 4/10 | ~3% dividend unverified by independent sources. 12.5% performance fee not widely disclosed. Below market. |

| Transparency | 5/10 | PPM available, Substack updates, whitepaper. But conflicting numbers across sources, no audited AI claims, truncated contract address. |

| Liquidity | 2/10 | No secondary market. $32/month on-chain volume. 1 active address. Blackout windows on redemptions. |

| Innovation | 7/10 | Rentvesting is genuinely new (if it launches). Grobot is interesting if unverified. Morpho integration ahead of competitors. |

| Regulatory | 4/10 | Accredited-only. No REIT election yet. No Reg A+ filing found. Political risk from Boston rent control initiatives. |

| Overall | 4.9/10 | Real project, real limitations. The limitations are more severe than they first appear, particularly on liquidity, yield verification, and regulatory status. |

Frequently Asked Questions

What is GromaCoin?

GromaCoin (GRO) is a tokenized share in the Groma Real Estate Trust, a private REIT that owns and operates small apartment buildings in Greater Boston. Each token equals one share. The token runs on Base and uses the ERC-3643 compliance standard. Current NAV is approximately $1.04.

Who is behind Groma?

Seth Priebatsch, who previously built LevelUp (sold to Grubhub for $390 million in 2018), and Chris Lehman, co-founder and policy architect. The team is approximately 40 people.

What yield does GromaCoin pay?

Groma claims approximately 3.3% annual dividend, paid quarterly, targeting 4-5% in 2026. Including estimated asset appreciation, the all-in return target is 7-11%. These figures are from Groma's own materials and have not been independently verified. A 1% management fee and 12.5% performance fee apply.

Can I sell GromaCoin?

As of May 2026, there is no secondary market for GRO tokens. Monthly on-chain transfer volume is $32. You can request redemption directly from the Trust at current coin value, subject to period limits, blackout windows, and the Trust's cash position. A Morpho lending market is expected in Q2 2026 that would allow borrowing against tokens as collateral.

Who can buy GromaCoin?

Currently restricted to accredited investors under SEC Regulation D Rule 506(c). Non-accredited investor access has been discussed but not launched.

How does Groma compare to traditional REITs?

Traditional public REITs offer average dividend yields of 4-5%, full liquidity (traded on stock exchanges), decades of operating history, and SEC oversight. Groma offers a lower unverified dividend yield, zero secondary liquidity, 218 holders, an unproven operating team in real estate, and a REIT election that has not yet occurred.

What is the difference between GromaCoin, GromaREIT, and Groma Fund I?

These are three separate investment vehicles. Fund I is a closed-end partnership (39 buildings). GromaREIT on Republic is a separate equity raise (47 buildings). The Groma Real Estate Trust (backing GromaCoin) is the open-ended REIT with 125+ buildings. Owning one does not give you claims on the others.

Daniil Kozin structures tokenized real-asset deals in Europe and writes the RWA Roast series to cut through the conference slides. Previous roasts: Centrifuge, Chainlink, Figure, Stellar, Kelp DAO, Syrup, Ondo, Canton. Full archive at daniilkozin.com/blog.

Sources:

- rwa.xyz — GromaCoin

- Groma Whitepaper

- Wefunder — Groma

- Republic — Groma

- Thesis Driven Deep Dive

- Groma Substack

- TechCrunch — Grubhub acquires LevelUp

- Castle Island Ventures Podcast EP.466

- Modern Treasury — Groma Partnership (March 2026)

- Groma PPM (February 2026)

Data as of May 26, 2026. RWA space moves fast. Always verify live metrics and do your own due diligence on credit pools.