This is the first time I am roasting a project that trades on NASDAQ.

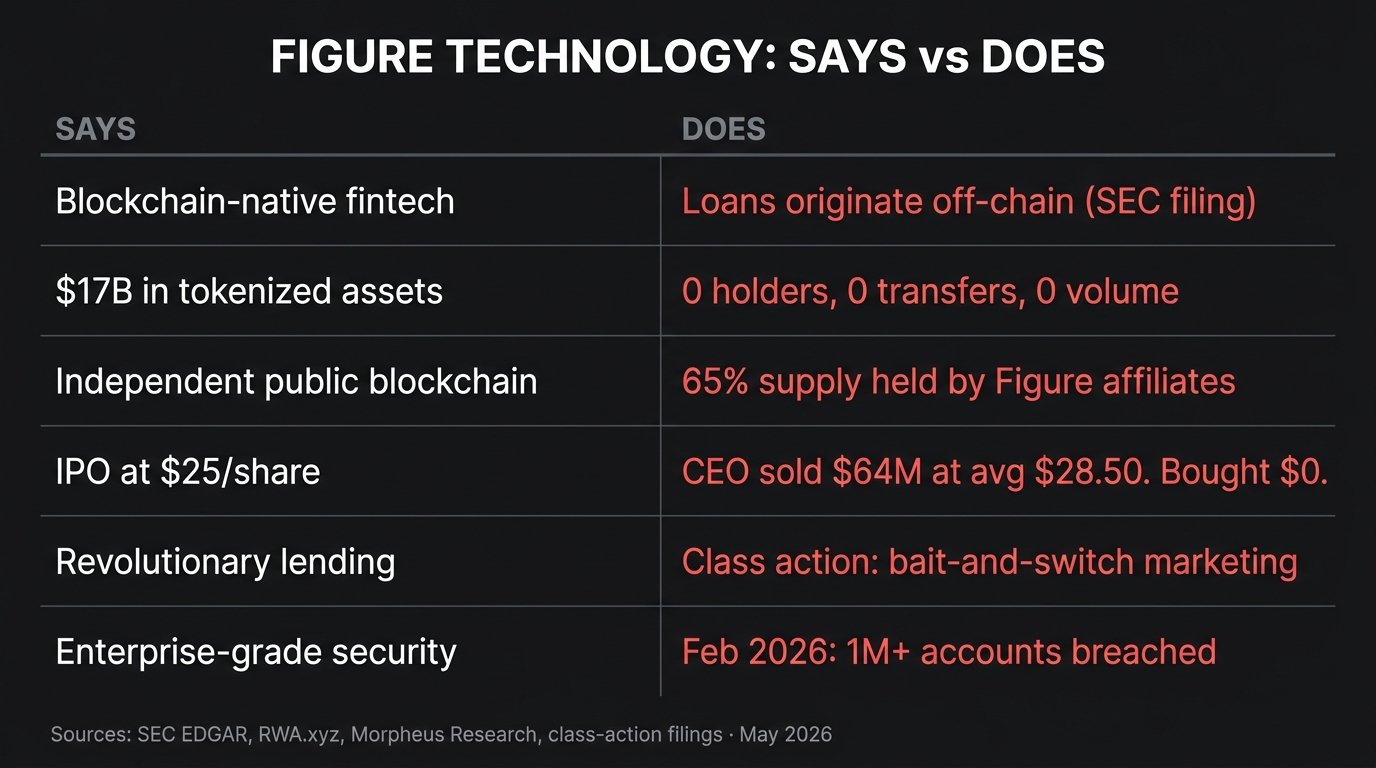

Figure Technology Solutions went public in September 2025 at $25 per share, raised roughly $787 million, and currently sits at a market cap that implies a 103% premium over comparable fintech lenders. The company also built its own Layer 1 blockchain called Provenance. And it uses that blockchain to tokenize its own home equity loans, reporting $17.05 billion in “represented asset value” on RWA.xyz.

But here is the number that does not make it into the press releases. RWA.xyz shows only $21.24 million in “distributed asset value” on the same page. Only 163 holders. Only 36 monthly active addresses. The $17 billion represents the face value of off-chain loans. The $21 million is what is actually distributed on the chain.

I went through SEC filings, on-chain explorer data, the Morpheus Research short report, class-action filings, DefiLlama and RWA.xyz metrics, and governance data. The gap between the story Figure tells and what the data shows is one of the widest I have seen in five episodes of this series.

The origin story: from SoFi scandal to Figure

To understand Figure, you need to understand Mike Cagney.

Cagney co-founded SoFi in 2011 and built it into one of the largest online lenders in America. By 2017, SoFi was valued at over $4 billion. Then the board forced Cagney out. The New York Times and Wall Street Journal reported allegations of sexual harassment, a toxic “frat house” workplace culture, and admitted sexual relationships with subordinates. One affair led to a settlement. Cagney resigned citing the distraction of litigation and media coverage.

Months later, in early 2018, Cagney founded Figure. Same industry. Same lending model. New blockchain angle.

His wife, June Ou, who served as CTO at SoFi, became a co-founder at Figure and now serves as Executive Director of the Provenance Foundation, the nonprofit that ostensibly governs the blockchain independently from the company. We will come back to that word “independently.”

Figure raised significant private funding before going public. DefiLlama shows $45.2 million in disclosed raises, though the total was reportedly much higher including undisclosed rounds. The IPO in September 2025 was upsized to 31.5 million shares at $25, raising approximately $787 million and valuing the company at roughly $5.3 billion. The stock peaked near $78 after the OPEN announcement, then settled around $36.

The pitch to public markets: Figure is not just a lender. It is a blockchain-native fintech that tokenizes real assets and trades them on its own chain. The blockchain is the moat.

The question this roast answers: is the blockchain actually the moat, or is it the marketing?

The business: HELOCs with a blockchain label

Figure’s core business is straightforward. It originates home equity lines of credit. It is the largest non-bank HELOC provider in America, with over $24 billion originated across its ecosystem and Q1 2026 marketplace volume of $2.9 billion, up 113% year over year.

The company is profitable. Q4 2025 showed 91% revenue growth with positive adjusted EBITDA and net income. 2024 full-year revenue was approximately $341 million. Cash position strong at roughly $1.2 billion. They authorized a $200 million share buyback.

These are real numbers. This is a real business. If Figure were just a fintech lender, the story would be simple: fast-growing, profitable, taking market share from banks in a $17 trillion home equity market.

But Figure does not want to be valued as a lender. It wants to be valued as a blockchain company. And that is where the problems start.

Here is how the tokenization actually works. Figure originates loans through a traditional Loan Origination System using CoreLogic, Plaid, and standard underwriting processes. The SEC filings confirm this. After the loan is originated, it gets tokenized as a “digital twin” on Provenance Blockchain using DART, their Digital Asset Registry Technology. The token represents the loan for custody, lien perfection, and secondary market trading.

The loans originate off-chain. The blockchain comes after. This is not blockchain-native origination. This is a traditional lender that stamps its loans onto a chain it controls for liquidity and reporting purposes.

A former employee quoted in the Morpheus Research short report put it plainly: the company has “the vision of a Porsche when all we have is a bicycle.”

Provenance Blockchain: the chain Figure built and controls

Provenance is a public proof-of-stake Layer 1 built on Cosmos SDK. Fast finality, four to five second blocks, custom modules for financial operations, CosmWasm smart contract support. On paper, it is a legitimate blockchain designed for real-world asset use cases.

In practice, it is Figure’s chain.

The TVL gap: three numbers, three different stories

Understanding what Provenance actually holds requires looking at three independent data sources, because each one tells a different story.

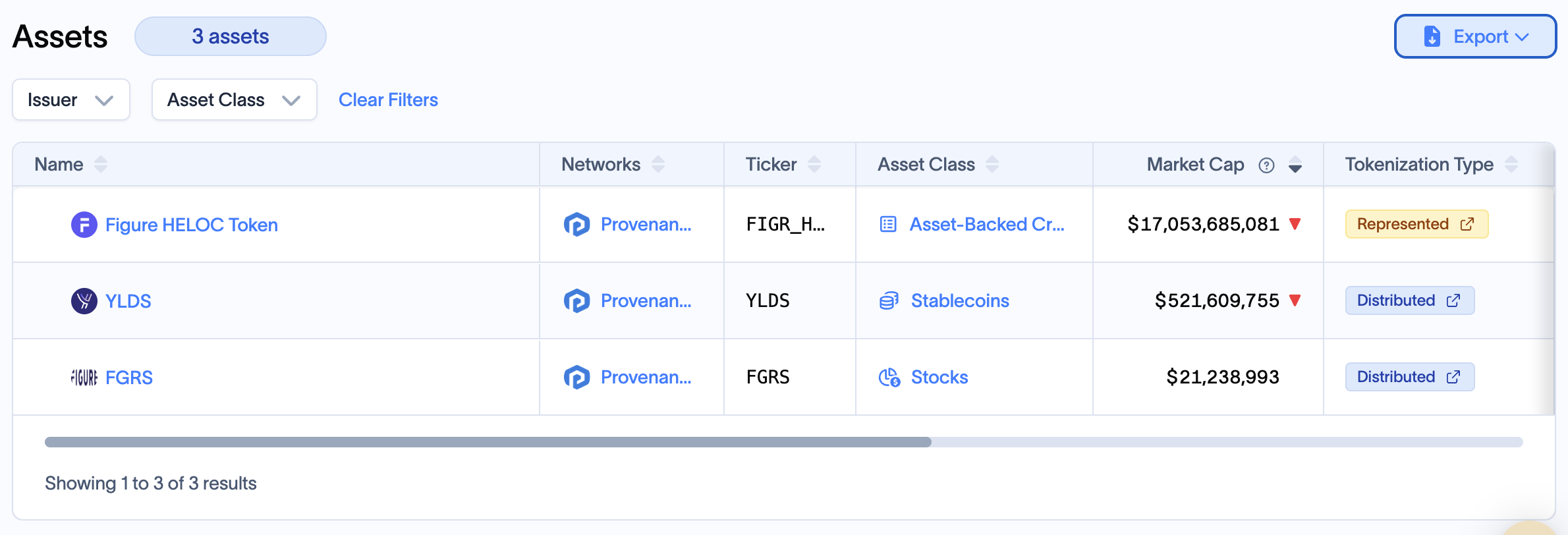

RWA.xyz lists Figure with exactly three assets. The breakdown tells you everything:

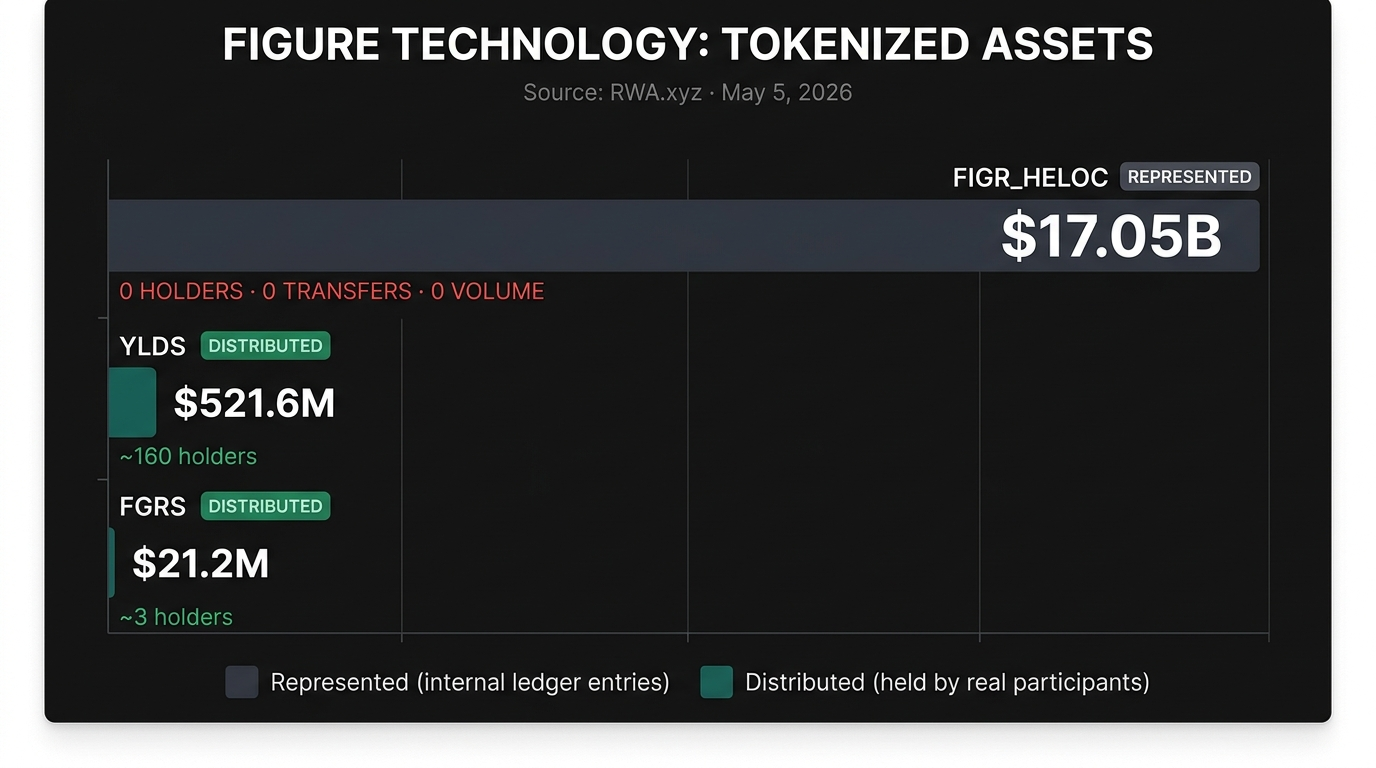

FIGR_HELOC (Figure HELOC Token): $17,053,685,081 in total value. Tokenization type: “Represented.” Holders: 0. Monthly transfer count: 0. Monthly transfer volume: $0.

Let me repeat that. The $17 billion asset that makes Figure one of the largest names in tokenized real-world assets has zero holders and zero transfers. Not low activity. Zero. The token supply matches the total value almost exactly at 17,053,685,080 tokens at $1.00 NAV. These are not tokens distributed to investors. These are internal ledger entries representing the face value of off-chain loans. Nobody holds them. Nobody trades them.

YLDS: $521,609,755. Tokenization type: “Distributed.” Asset class: Stablecoins. This is the SEC-registered yield product and it is legitimately distributed to actual holders.

FGRS: $21,238,993. Tokenization type: “Distributed.” Asset class: Stocks. This is the OPEN equity product.

So Figure’s actual distributed, held-by-real-people tokenized assets total roughly $543 million. Not $17 billion. The $17 billion is a represented value of off-chain loans stamped onto the chain with zero external holders.

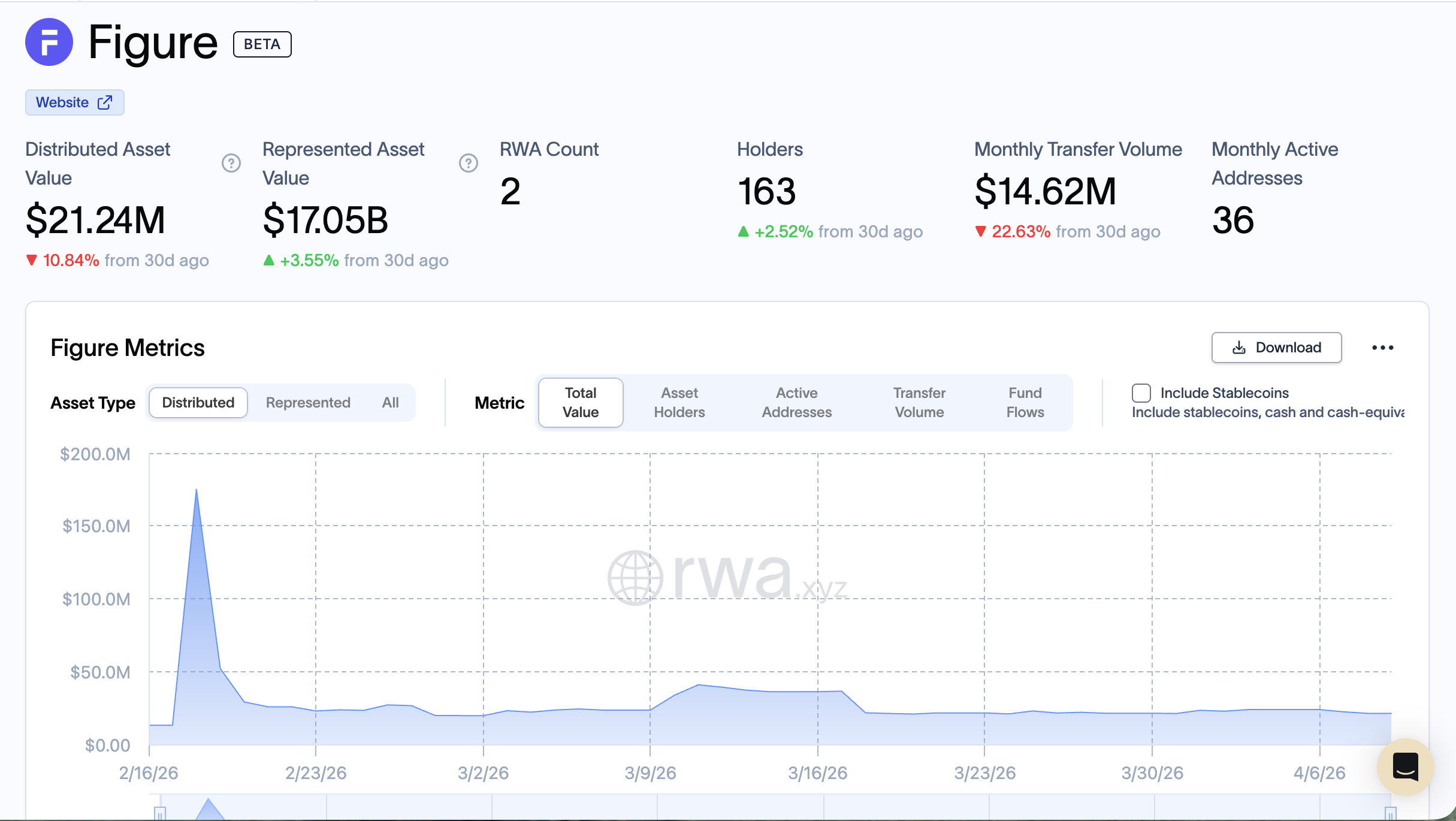

RWA.xyz classifies this correctly. The platform-level summary shows $17.05 billion in “represented asset value” and $21.24 million in “distributed asset value” (down 10.84% in 30 days). The Provenance network page shows 163 RWA holders, 36 monthly active addresses, and $14.62 million in monthly transfer volume (down 22.63%).

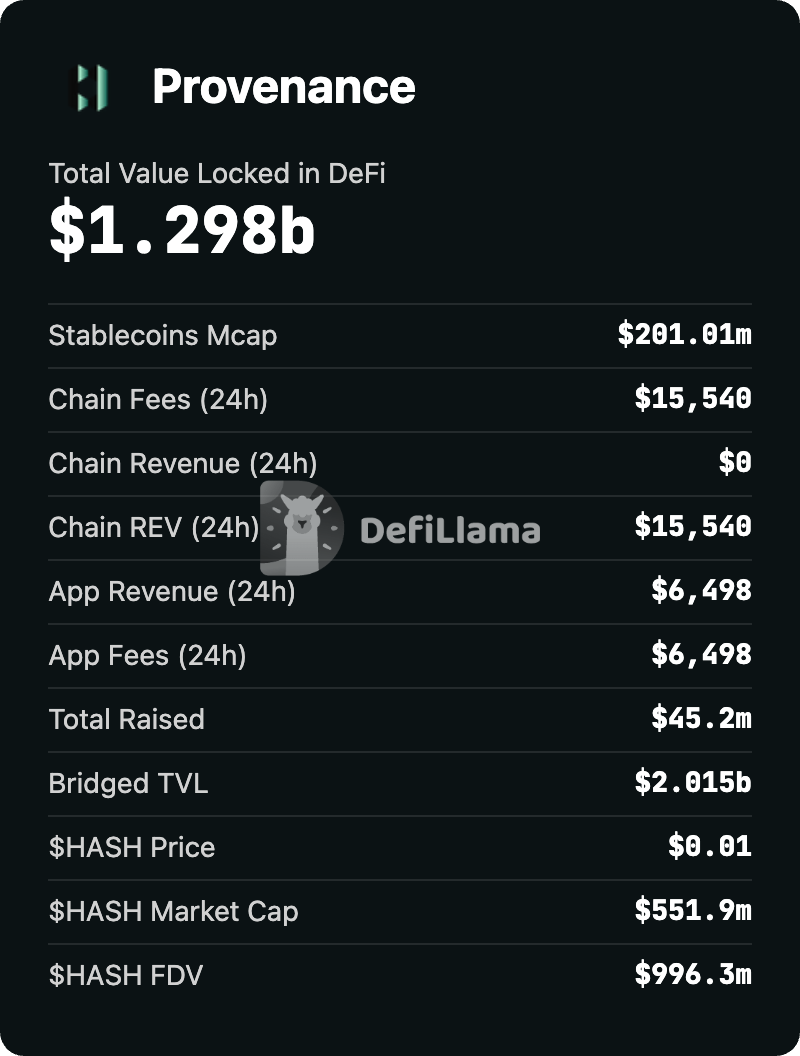

DefiLlama shows Provenance at $1.298 billion in DeFi TVL, with $2.015 billion in bridged TVL. This has grown from near zero in mid-2025, driven largely by YLDS and stablecoin activity.

A platform citing $17 billion in tokenized assets has zero holders on its flagship product and 36 monthly active addresses across everything. That is not a decentralized financial ecosystem. That is one company’s loan ledger on a chain it controls.

The HASH token

HASH is the native staking and governance token. Here is what the data shows as of May 2026:

HASH price: $0.01. Market cap: $551.9 million. Fully diluted valuation: $996.3 million. That is not a typo. The token that powers a chain claiming $17 billion in assets is worth one cent.

Ten accounts control approximately 78% of all bonded HASH. Figure and Cagney-affiliated entities hold roughly 65% of the total HASH supply. Most validators are undercapitalized, with many having minimal self-stake averaging around $23 after delegation. Two accounts could theoretically halt the network based on CometBFT consensus documentation.

In January 2026, a community vote gave Figure execution control over the Provenance Foundation. Cagney’s wife runs the foundation. The company that builds on the chain now also runs the chain’s governance body.

Chain economics

DefiLlama reports Provenance chain fees at $15,540 per day. Chain revenue: $0. That means all fees go to validators and stakers but the protocol itself captures nothing. App fees add another $6,498 per day.

For context: $15,540 in daily chain fees annualizes to roughly $5.7 million. On a token FDV of $996 million, that gives you a price-to-fees ratio of 175. Not the worst in crypto, but for a chain where one company generates most of the activity, the fee revenue tells you how much the rest of the ecosystem actually uses this chain. Not much.

RWA.xyz reports stablecoin market cap on Provenance at $521.61 million (down 15.72% in the last 30 days), with 3,298 stablecoin holders and $9.29 billion in 30-day stablecoin transfer volume. The stablecoin transfer volume is high relative to other metrics, likely driven by Figure’s own YLDS product and institutional settlement operations. But 3,298 stablecoin holders on a chain whose flagship RWA product has zero holders tells you who is actually on this chain.

The explorer glitch

In March 2026, the Provenance blockchain explorer displayed $390 quadrillion in assets for a single broker account. The error persisted for approximately two weeks before being fixed. For a chain that markets itself as institutional-grade infrastructure for real financial assets, a display error of that magnitude raises questions about data integrity and monitoring.

The product suite beyond HELOCs

Figure has expanded beyond basic HELOC tokenization:

Democratized Prime pools allow on-chain lending and borrowing against HELOC pools. Approximately $368 million in matched offers. Some pools pay yields above warehouse line rates, around 8.7% versus 5.5% on traditional lines. The question for investors: who is subsidizing that spread, and for how long?

YLDS is an SEC-registered yield-bearing token, essentially a tokenized money market product. Roughly $598 million in circulation as of Q1 2026. This is probably the most legitimate blockchain product Figure has built, because it actually uses the on-chain rails for something that benefits from them.

OPEN (On-Chain Public Equity Network) launched around January 2026 for on-chain stock lending and equity issuance. Figure calls it the first public equity product native to a public blockchain. BitGo and Jump Trading are partners. But critics note daily volume under $60,000 in some analyses. That is not adoption. That is a proof of concept with a press release.

The skeletons: lawsuits, selling, and a CFO problem

This section is longer than usual because there is more here than I have seen in any previous roast.

Class action #1: bait-and-switch HELOCs (2024)

A class action (Lee Ward et al.) alleges Figure marketed HELOCs as flexible revolving lines of credit but required borrowers to draw the full amount at closing. That makes it functionally a closed-end loan with higher fees and interest than what was advertised. Consumer complaints to the CFPB and Better Business Bureau describe “deceptive” and “predatory” practices, inaccurate payoff amounts, and improper fees.

This is not a technicality. A HELOC that requires full draw at origination is not a line of credit. It is a lump-sum loan with a different name. Full-draw utilization above 95% is linked to 4x higher delinquency risk according to third-party data. The product design drives the credit risk.

Class action #2: data breach (February 2026)

Mardikian v. Figure Lending alleges a cyber incident exposed customer and lead personally identifiable information across reportedly over one million accounts. The complaint claims inadequate employee training, insufficient security protocols, and substandard safeguards. For a company handling billions in home equity data, this is not a minor issue.

Insider selling

Post-IPO, CEO Mike Cagney sold approximately $64 million in shares at an average price of $28.50. He has made no purchases. Another executive sold roughly $53 million. Public statements from Cagney hyping the stock price while selling were criticized as inconsistent. A UCC filing suggests an undisclosed 2-million-share pledge that was not in public disclosures.

When the founder sells $64 million and buys nothing, you can read his conviction in the numbers.

The CFO problem

CFO Macrina Kgil’s official biography omits her prior role at GPB Capital. GPB Capital was charged by the SEC in 2021 in connection with what regulators described as a $1.7 billion Ponzi-like scheme. Kgil was allegedly “instrumental” in operations there. Her Figure bio does not mention this.

I am not saying guilt by association. I am saying that when your CFO’s biography has a hole in it the size of an SEC enforcement action, investors deserve to know.

Credit quality: the numbers behind the growth

Figure’s loan book is growing fast. But so are the delinquencies.

Critics cite a 5.46% delinquency rate in 2025, which is higher than some peers. Bank of America’s HELOC delinquencies were declining over the same period. The full-draw model, where borrowers must take the entire credit line at once, concentrates risk in ways that traditional revolving HELOCs do not.

The Morpheus Research short report (published April 16, 2026, with a disclosed short position) conducted a four-month investigation and labeled Figure “a risky home equity lender masquerading as a blockchain innovator.” They cited SEC admissions that the Loan Origination System is not blockchain-dependent, former employee interviews, spreadsheet usage in what should be automated audits, and credit data suggesting underwriting is looser than marketing implies. DBRS data showed 11%+ valuation divergence in some lending pools.

Figure’s securitizations have historically received AAA ratings. The loans perform. But the question is whether growth at this pace, with these incentive structures, can maintain credit quality through a full housing cycle. We have not tested that yet. And with Q1 2026 earnings expected May 11-12, the next delinquency data will be closely watched.

The valuation problem

Even setting aside the blockchain narrative, the stock price carries a significant premium.

Figure trades at roughly 103% above fintech peer valuations on forward earnings metrics and 220% premium on price-to-book. The market is pricing in blockchain optionality on top of the lending business. If you strip out the blockchain premium and value Figure purely as a lender, the stock is expensive relative to SoFi, Rocket Mortgage, and traditional HELOC originators who are growing into this market aggressively.

Competition is intensifying. SoFi and Rocket Mortgage are both expanding HELOC offerings. These are not small players. If Figure’s market share advantage comes from speed of origination (which they attribute to blockchain), but the origination actually happens on a traditional system, then the competitive moat may be thinner than investors assume.

The $200 million share buyback authorization is a positive signal. The strong cash position of $1.2 billion provides runway. But buybacks funded by IPO proceeds while insiders sell into the same market is a pattern worth watching.

My verdict: the same four questions

1. Does the yield survive real math?

FIGR_HELOC tokenized assets generate yield from actual borrower payments on home equity loans. This is real cash flow from real mortgages. Unlike many DeFi yield sources, the underlying economics are straightforward: people borrow against their homes and pay interest.

But the delinquency rate is rising. The full-draw model concentrates risk. And the yields offered on Democratized Prime pools (8.7%) exceed what the underlying warehouse lines cost (5.5%), which means someone is subsidizing the spread, likely to attract volume for the blockchain narrative.

The yield is real. The question is whether it stays real through a housing downturn with a 5.46% and rising delinquency rate on a portfolio that grew 113% in one year.

Conditional pass. Real yield, real risk. The pace of growth without a cycle test is the concern.

2. What do you actually own?

If you buy FIGR stock: you own equity in a profitable, growing fintech lender with a blockchain division. That is legitimate.

If you buy HASH at $0.01: you own a governance token for a chain controlled by the company that built it, where 10 accounts hold 78% of staked supply, FDV is $996 million on $15,540 per day in fees, and the token has lost 92% since inception. The governance is not meaningfully decentralized. You do not control anything.

If you hold FIGR_HELOC tokens: you hold digital representations of loans originated off-chain by a traditional process. Your claim runs through Figure’s legal structure, not through smart contract enforcement.

Pass for FIGR equity. Fail for HASH. The stock is a real investment in a real company. The token is a centralized governance instrument for a chain that does not need your governance.

3. Can you exit?

FIGR trades on NASDAQ with institutional liquidity. No exit issues for the stock.

HASH has a market cap of $551.9 million but minimal daily volume. If you own any meaningful position, you cannot exit without moving the market. The token is not listed on major centralized exchanges. Exit is theoretical for any real size.

FIGR_HELOC tokens trade on Figure Connect, which is Figure’s own marketplace. Liquidity depends on Figure’s market-making and institutional buyer interest. This is not Uniswap. You cannot exit permissionlessly. You exit when Figure’s marketplace has a buyer.

Pass for FIGR stock. Fail for HASH. Conditional for FIGR_HELOC (depends on Figure Connect liquidity remaining active).

4. Skin in the game?

The CEO sold $64 million in stock post-IPO and bought nothing. The CFO has an undisclosed history with a firm charged by the SEC. The company’s founder was ousted from his previous company for workplace conduct issues. The chain’s foundation is run by the CEO’s wife and controlled by the company since January 2026.

Every structural decision concentrates more control with Cagney and his inner circle. That is either supreme confidence or supreme self-dealing. The $64 million in sales with zero purchases suggests the latter.

Compare this to the Syrup roast: Sid Powell rebuilt from $54 million in defaults with $6.4 million in total funding. That is skin in the game. Selling $64 million while publicly pumping the stock is the opposite.

Fail. The insider selling pattern contradicts the long-term conviction narrative.

Figure Technology is a legitimate, profitable, fast-growing home equity lender. The business works. Revenue is real. Loans are real. Growth is impressive.

But the blockchain story does not match the data. Loans originate off-chain. The chain is controlled by the company. RWA.xyz shows $17.05 billion in “represented” value but only $21.24 million “distributed” and only 163 holders with 36 monthly active addresses. DefiLlama shows $1.3 billion in DeFi TVL. The governance token sits at $0.01 with a 92% decline from inception. Chain fees are $15,540 per day with $0 in protocol revenue. These are the numbers of a chain that one company uses for its own operations, not the numbers of a thriving decentralized ecosystem.

The leadership issues would give any institutional investor pause. A CEO ousted for misconduct, a CFO with an undisclosed SEC-adjacent history, $64 million in insider sales with zero purchases, two active class actions, rising delinquencies, and a foundation “independence” that evaporated in January 2026.

If you are investing in FIGR as a high-growth HELOC lender with a blockchain optionality kicker and you are comfortable with the credit cycle risk and leadership history, there is a case to be made. The business metrics support it. If you are investing because you believe Provenance is the future of decentralized real-world asset infrastructure, look at the staking concentration, the HASH price, the 36 monthly active addresses, and the $17B vs $21M gap. Then decide whether one company’s loans on one company’s chain means what you think it means.

Sources

- SEC EDGAR: Figure Technology Solutions filings

- RWA.xyz: Figure platform data

- RWA.xyz: Provenance network data

- Morpheus Research: Figure Technology short report (April 16, 2026)

- NASDAQ: FIGR stock data

- Provenance Blockchain Explorer

- DefiLlama: Provenance chain data

- NYT: SoFi CEO ouster coverage (2017)

- Lee Ward et al. v. Figure Lending (class action)

- Mardikian v. Figure Lending (data breach class action, W.D.N.C., February 2026)

- SEC: GPB Capital enforcement action (2021)

- CoinGecko: HASH token

This is the fifth in a series where I take a real project and run the same due diligence I would use before putting my own money in. To get the next one first, join the Telegram or follow me on LinkedIn.

Nothing in this article is investment advice. I do not hold FIGR stock, HASH tokens, or FIGR_HELOC positions. I have no financial relationship with Figure Technology Solutions. The Morpheus Research report cited herein was published by a firm with a disclosed short position. Do your own research.