Centrifuge has been in the RWA conversation since before most people knew what RWA meant. They tokenize private credit, invoices, CLOs, treasuries, and now even S&P 500 exposure. Janus Henderson runs funds through them. Coinbase just made them preferred tokenization infrastructure on Base. TVL is $1.57 billion.

I spent a week going through the on-chain data, the income statements, the token economics, and the fund structures. What I found is a protocol that is genuinely useful, backed by serious institutions, and almost entirely unable to capture value for the people who hold its token.

What Centrifuge Actually Does

If you are not deep in RWA infrastructure, here is the simple version.

Centrifuge lets asset managers and originators put real-world assets on a blockchain. A lending company in Kenya has invoices worth $5 million. A European firm has a portfolio of corporate loans. An asset manager wants to run a tokenized treasury fund. Centrifuge gives them the tools to wrap those assets into on-chain tokens, with legal structures (SPVs), compliance (KYC/AML), and reporting built in.

Think of it as a factory for tokenized funds. You bring the asset, Centrifuge provides the conveyor belt.

The key pieces: asset pools where investors deposit capital, institutional vault tools that handle NAV reporting and lifecycle management, and connections to DeFi protocols like Aave, Morpho, and Sky so those tokenized assets can actually be used as collateral or traded.

They started on their own Polkadot-based chain (Centrifuge Chain) and have since expanded across Ethereum, Avalanche, Base, Solana, Stellar, and others. The original Tinlake platform that processed SME lending pools has evolved into a multi-chain institutional toolkit.

The Good: Real Assets, Real Partners, Real Scale

The numbers are not small.

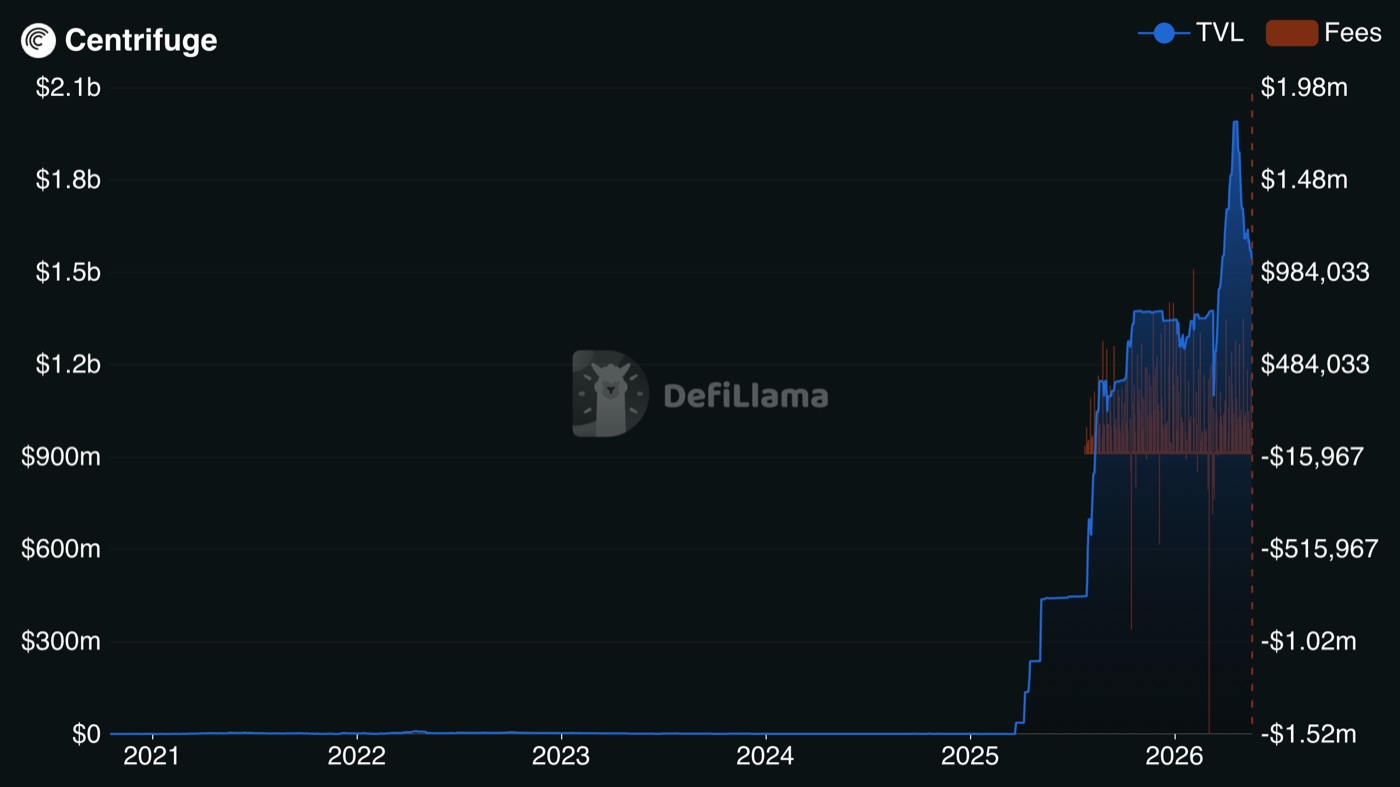

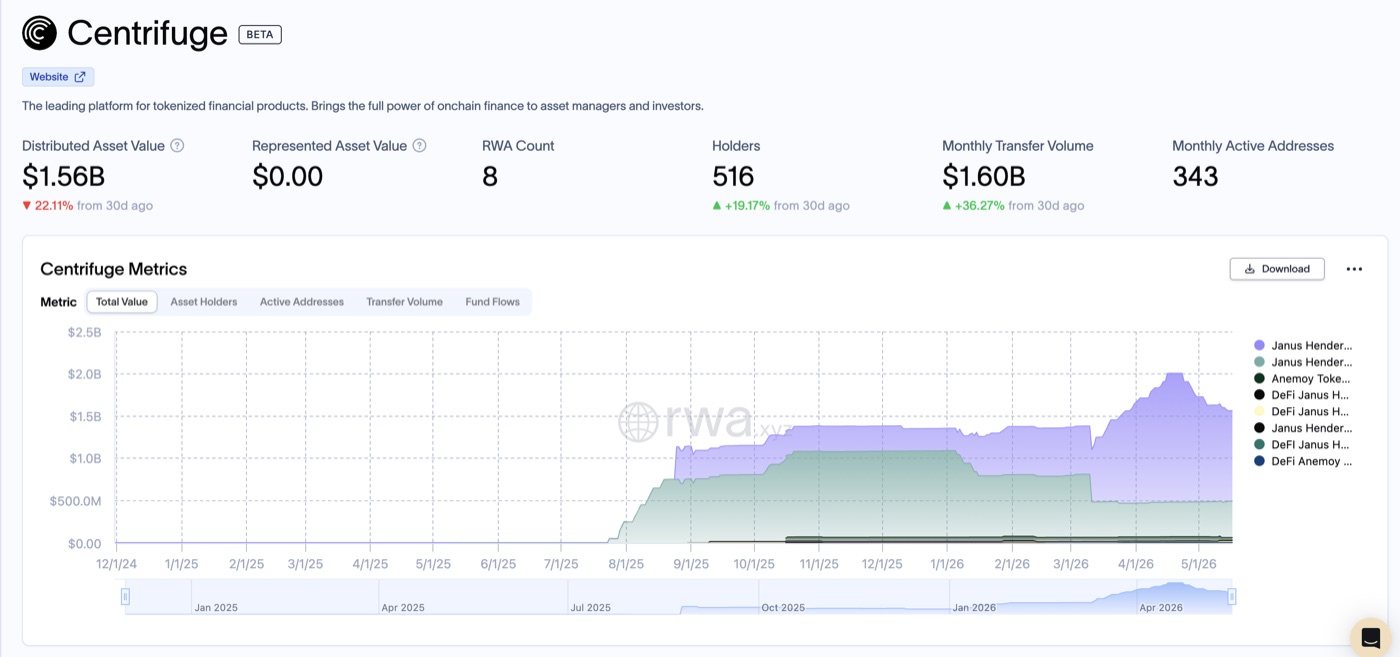

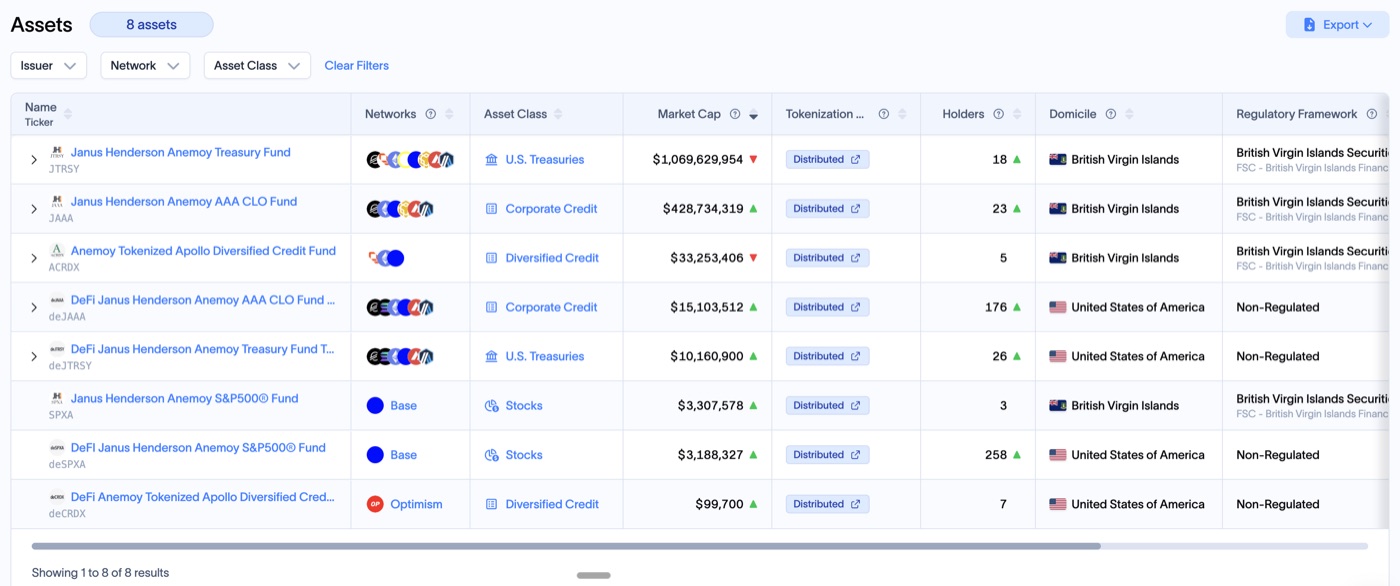

$1.57 billion in TVL across 10 networks. Ethereum holds 79% of that ($1.2 billion), Avalanche carries 17% ($258 million). Over 1,768 assets have been tokenized through the platform historically. Monthly transfer volume of $1.71 billion.

The biggest products on the platform are institutional. The Janus Henderson Anemoy Treasury Fund (JTRSY) holds $1.07 billion alone. The Janus Henderson AAA CLO Fund (JAAA) holds $428 million. There is an Anemoy Apollo Diversified Credit Fund at $33 million. A tokenized S&P 500 fund just launched. Janus Henderson manages over $380 billion globally. When a firm like that commits to a tokenization platform, it is not a pilot.

The Coinbase partnership announced May 5, 2026 is significant. Coinbase took an equity stake (described as seven figures), named Centrifuge preferred tokenization backbone, and committed to using it as the default issuance layer for tokenized assets across Base. Coinbase Ventures had already participated in earlier rounds including a $15 million Series A in 2024.

Three days before this article, Grove launched Basin, a liquidity infrastructure that offers up to $1 billion in committed daily liquidity for instant stablecoin redemptions of tokenized RWAs. This is a facility, not actual daily volume. Centrifuge is one of the tokenization partners, alongside Securitize. BlackRock and Janus Henderson are the initial asset management partners. This addresses one of the biggest pain points in tokenized assets: getting your money out without waiting days for settlement.

Real funds. Real AUM. Real institutional names.

The Bad: A 27x Revenue Multiple

Now for the part that matters if you actually hold CFG.

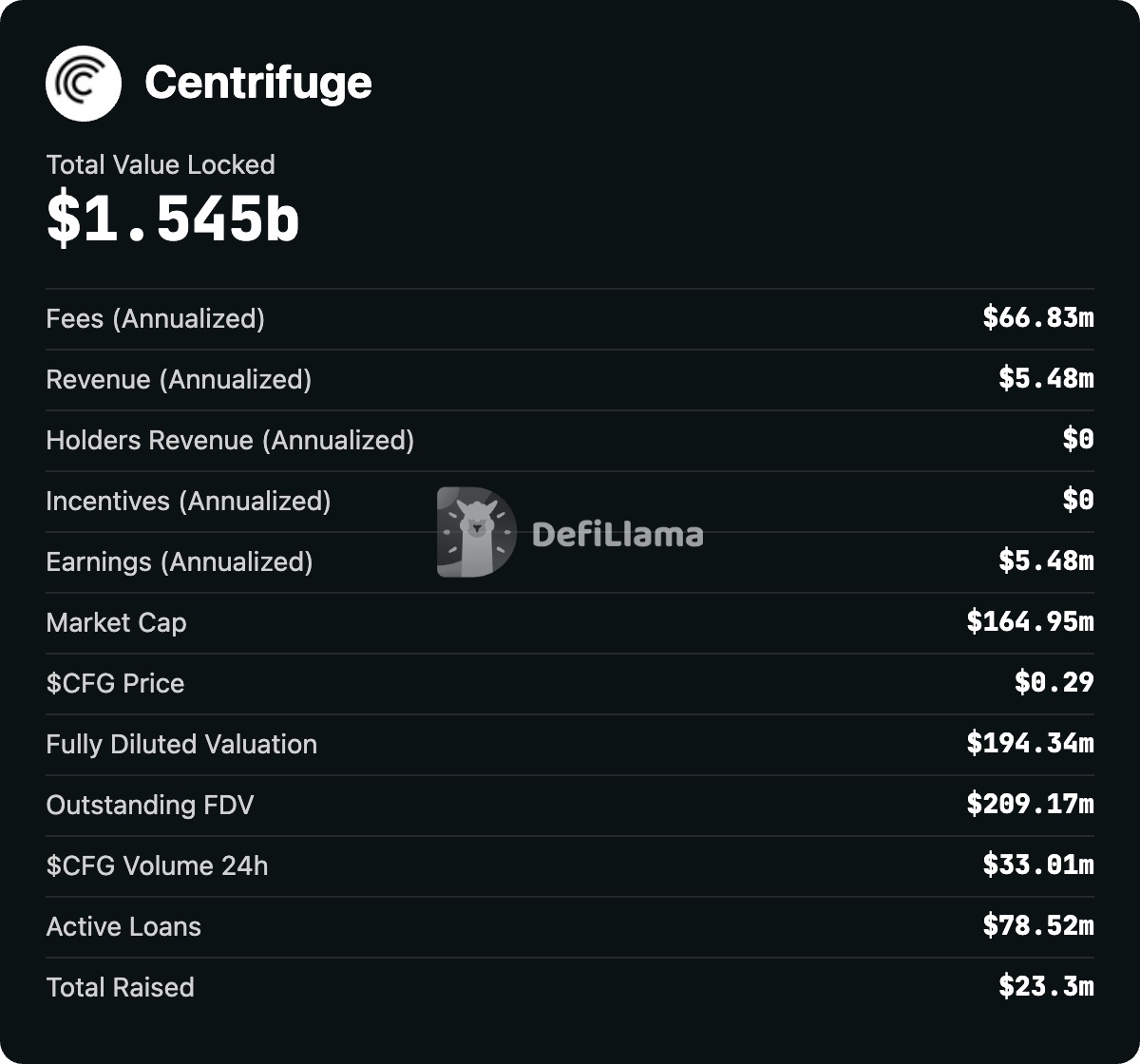

Centrifuge generates $69 million in annualized fees. That sounds impressive until you look at where those fees go. Of that $69 million, only $5.5 million reaches the protocol as revenue. The rest flows to asset originators, managers, and the funds themselves.

Market cap: $150 million. CFG price: $0.26. That gives you a 27x multiple on protocol revenue. Not catastrophic compared to some crypto valuations, but not cheap for what amounts to infrastructure plumbing.

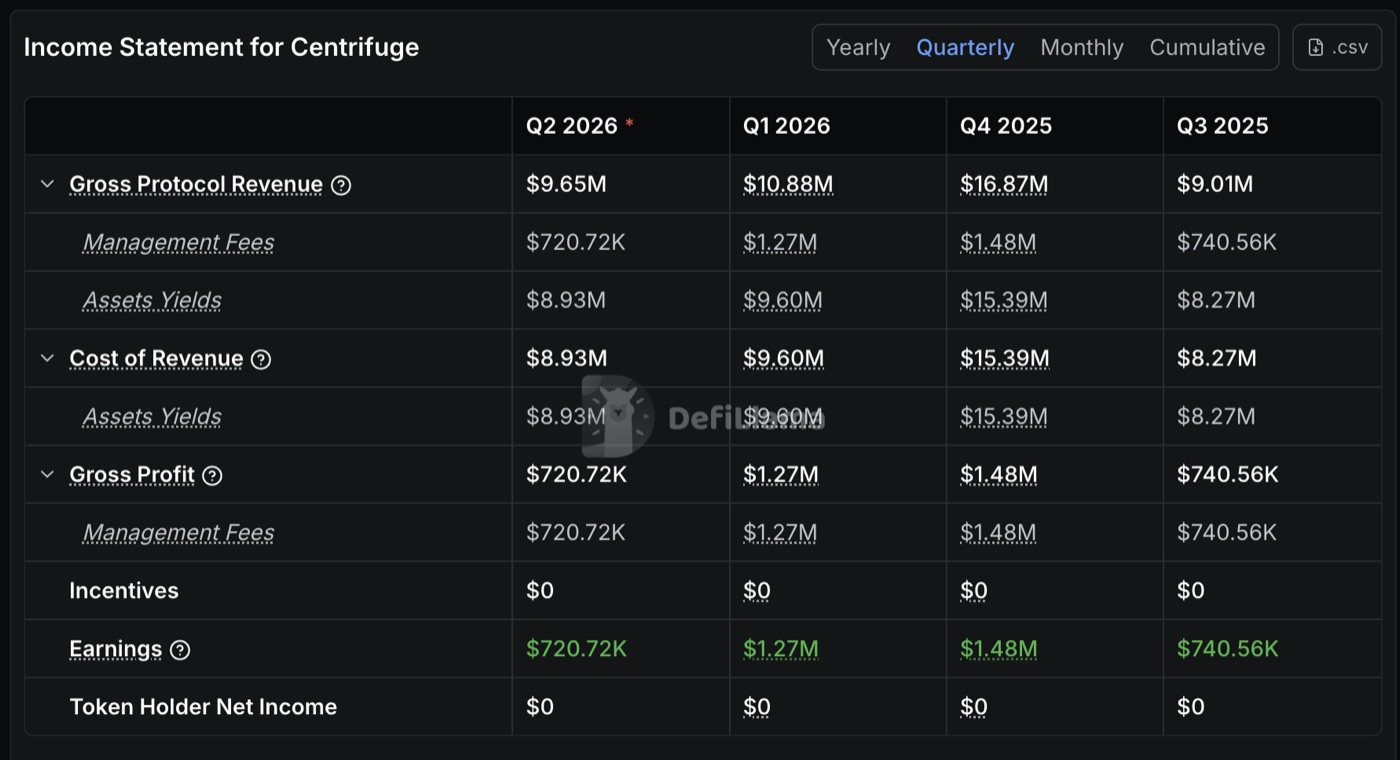

Look at the income statement quarter by quarter. Q4 2025 was the best quarter: $1.48 million in protocol earnings. Q1 2026: $1.27 million. Q2 2026 so far (partial quarter): $707,000. The trajectory is flat to declining. Cumulative earnings across the last 3 full quarters plus partial Q2 total roughly $4.2 million.

The protocol's take rate on TVL it manages is 0.35%. For context, traditional fund administration platforms charge 5 to 15 basis points and have much higher revenue per dollar of AUM. Centrifuge captures less than most of its TradFi equivalents, while carrying the additional complexity of multi-chain smart contract infrastructure.

The Concentration Problem Nobody Talks About

This jumped out at me more than anything else in the data.

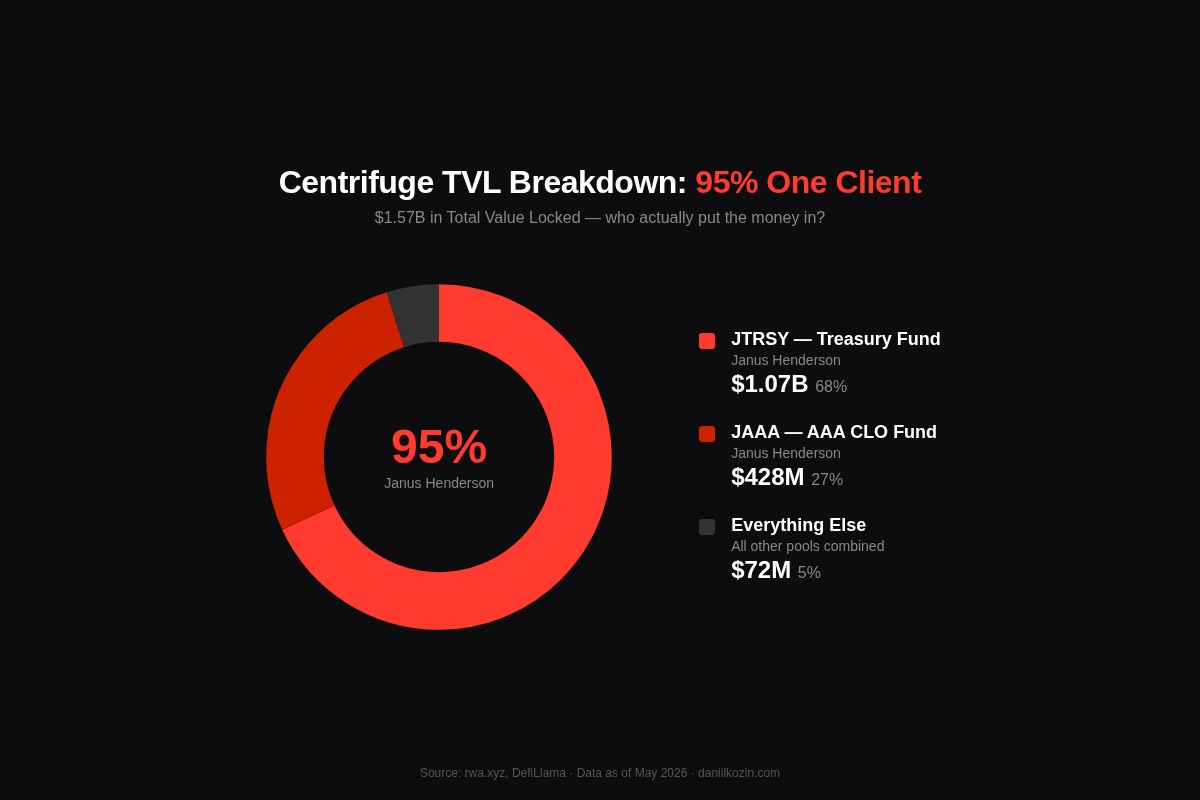

518 holders across the entire platform. $1.57 billion in TVL. That is an average of $3 million per holder.

But the distribution is far more skewed than that. The top 2 funds (JTRSY and JAAA, both Janus Henderson) account for $1.5 billion. That is 95% of the total TVL sitting in products from a single asset manager.

If Janus Henderson decides to move its tokenized funds to a different platform, Centrifuge loses 95% of its TVL overnight. The protocol's headline number, the one that justifies its market cap and attracts new investors, depends almost entirely on one client relationship.

This is not a theoretical risk. In institutional finance, platform migrations happen regularly when better terms or technology appear. Securitize, Maple, and a dozen newer platforms would all be happy to host Janus Henderson's funds.

The TVL vs. Active Loans Gap

Active loans on the platform: $78.66 million. Total TVL: $1.57 billion. That means roughly 95% of the capital in Centrifuge is sitting in tokenized funds and treasuries, not actively lending.

Is that bad? Not necessarily. If you are an asset manager running a tokenized treasury fund through Centrifuge, the capital is being productively deployed inside the fund. It is just not generating lending spread for the protocol.

But it raises a question about what Centrifuge actually is. Is it DeFi infrastructure that enables on-chain lending and composability? Or is it a TradFi wrapper that gives institutional funds an on-chain address? The 95/5 split between passive fund AUM and active lending suggests it is mostly the latter right now.

The DeFi composability features exist. Centrifuge assets can plug into Aave, Morpho, and Pendle. But the majority of value locked is behaving like a tokenized ETF wrapper, not like a DeFi lending pool. For CFG investors, the question is whether TVL from passively held institutional funds translates into protocol revenue growth. So far: barely.

The Token Problem

CFG has the same disease that plagues most RWA infrastructure tokens.

Total supply: roughly 692 million CFG. Original allocation gave 29% to core contributors, 20% to community grants, 18% to early backers. In 2025, governance proposal CP149 added 115 million new tokens: 15 million unlocked immediately, the remaining 100 million vesting through April 2029. Team tokens (14% of supply) vest through March 2030. There is 3% annual inflation accruing to the treasury.

On one side: ongoing unlock pressure from multiple directions. On the other side: no buyback, no meaningful fee share to holders, no burn mechanism. Holders Revenue on DefiLlama reads $0. Token Holder Net Income reads $0. Every quarter. Consistently.

CFG is primarily a governance and staking token. Proposals for protocol fee distribution have been discussed in governance forums for over a year. Implementation has lagged. Even if the fee switch happens tomorrow, the economics are thin. $5.5 million in annual revenue split across 692 million tokens equals less than $0.008 per token per year. At the current price of $0.26, that is a 3% yield before any operational costs.

The Coinbase and Binance listings drove price spikes. But listing momentum fades. The underlying value capture mechanism is the chronic weakness. TVL grows, partners accumulate, and CFG holders are still at $0 in distributions.

Credit Risk: Real, Not Theoretical

Centrifuge originated in on-chain credit markets. The legacy Tinlake platform processed real lending pools for SME borrowers in emerging markets. That is a fundamentally different risk profile from holding tokenized US Treasuries.

The current product mix is heavily institutional (Janus Henderson funds dominate the TVL), which reduces credit risk. But the platform still hosts diversified credit pools and the architecture expects some defaults as normal business. Junior tranches (TIN tokens) absorb losses first, protecting senior tranches (DROP tokens). The structure is sound, but it is not default-proof.

KYC/AML whitelisting protects institutional compliance but limits retail access and DeFi composability. If you want to use a Centrifuge asset as collateral in a permissionless lending pool, the whitelisting requirement creates friction that fully permissionless assets do not have.

Smart contract risk exists across the multi-chain deployment (10 networks). Legal enforcement of SPV structures across jurisdictions is not free or instant. If an originator in a developing country defaults on their pool, recovery involves real-world legal proceedings, not just on-chain liquidation.

Competition

Centrifuge competes in a crowded and growing space.

Ondo dominates the pure Treasury/yield vertical. Simpler product, stronger retail brand, larger market cap ($3B+). If you want tokenized Treasury exposure, Ondo is the name most people think of first.

Maple Finance has a cleaner institutional lending model with more direct value accrual. Maple implemented buyback mechanisms and reported $2.5 million in quarterly protocol revenue in Q1 2026. On a smaller TVL base, Maple captures more revenue per dollar managed.

Securitize is the default name for large-scale tokenized securities with regulatory clearance (broker-dealer license). They handle BlackRock's BUIDL fund. In terms of regulatory positioning, Securitize is ahead.

Where Centrifuge wins: diversification of asset classes (credit + funds + CLOs + equities), DeFi composability (assets plug into Aave, Morpho, Pendle), and multi-chain presence. They are a toolkit, not a single product. For an asset manager who wants to launch a tokenized fund with legal wrappers and plug it into DeFi, Centrifuge is one of the few platforms that can handle the full stack.

Where they lose: simplicity, token economics, and brand clarity. If you ask a crypto investor what Ondo does, they can answer in one sentence. If you ask what Centrifuge does, the answer takes a paragraph. In a market that rewards simplicity, that is a real disadvantage.

The Same Four Questions

I ask these in every RWA Roast. They cut through the noise.

1. Does the yield survive real math?

The funds on Centrifuge (JTRSY, JAAA) generate real yield from real assets (Treasuries, CLOs). Those yields are legitimate and comparable to their TradFi equivalents. For the protocol itself: 0.35% take rate on $1.57B TVL producing $5.5M revenue. Thin but real. For CFG holders: zero yield, zero distributions. Platform: Pass. Token: Fail.

2. What do you actually own?

If you invest through a Centrifuge pool, you own tokenized shares in a legally structured SPV. There is real legal recourse. This is one of Centrifuge's genuine strengths. If you buy the CFG token, you own a governance token with no claim on protocol revenue, no share of fees, and no equity in the company. Pool investor: Pass. Token holder: Fail.

3. Can you actually exit?

Fund investors can redeem through standard processes. The Grove Basin partnership (up to $1B daily liquidity facility) should improve settlement speed significantly. For CFG token holders, liquidity is decent ($10.4M daily volume) but the persistent unlock schedule creates steady sell pressure. Pool investor: Pass. Token: Conditional pass.

4. Skin in the game?

The Centrifuge team holds 14% of tokens vesting through 2030. Coinbase took an equity stake. Janus Henderson is running real AUM. The people building this have real exposure. Whether that exposure is aligned with CFG token holders specifically is less clear, since the equity and the token are separate instruments. Conditional pass.

The Scorecard

| Category | Score | Justification |

|---|---|---|

| Technology and Compliance | 8/10 | SPVs, legal wrappers, multi-chain EVM, 21+ audits. Institutional-grade. Compared to Chainlink (8/10 for battle-tested oracle infra), equivalent quality. |

| Revenue and Value Accrual | 4/10 | $5.5M protocol revenue, 27x P/S, 0.35% take rate. Better than Chainlink (2/10, 100x P/S) but still thin for the TVL it manages. $0 to holders. |

| Institutional Adoption | 7/10 | Janus Henderson ($1.5B in funds), Coinbase equity, Grove/Basin partnership. Real production, not pilots. Higher than Chainlink (5/10, mostly pilots). BUT: 95% concentration in 1 client. |

| Tokenomics | 3/10 | Ongoing unlocks through 2030, 3% inflation, no burn, no fee share, $0 holder net income. Same structural weakness as Chainlink (3/10). |

| Competition | 6/10 | Wins on asset diversity and DeFi composability. Loses to Ondo on simplicity, Maple on revenue capture, Securitize on regulatory moat. |

| RWA Relevance and Moat | 7/10 | Diversified toolkit with DeFi connectivity. But the 95% Janus Henderson concentration means the "moat" depends on one relationship. Adjusted down from 8 to 7 for concentration risk. |

| Overall | 5.5/10 | Real infrastructure doing real work. The concentration risk and zero token value capture prevent a higher score. |

The Verdict

Centrifuge is one of the most credible RWA infrastructure protocols in the space. The compliance layer works. The institutional partnerships are real. The DeFi integrations exist and function. If you are an asset manager looking to tokenize a fund, this platform deserves evaluation.

The problem is not what Centrifuge does. The problem is what CFG captures. $1.57 billion flows through the platform. $5.5 million reaches the protocol. $0 reaches the token holders. The governance proposals for fee distribution have been circulating for over a year with no implementation. And 95% of the TVL comes from a single client.

The Coinbase partnership, the Basin liquidity network, and the expanding asset classes could change the trajectory. But right now the numbers say one thing clearly: the infrastructure works, and the token is still looking for a reason to exist.

Frequently Asked Questions

Is Centrifuge a good investment?

It depends on what you are investing in. If you are putting capital into a Centrifuge pool (like the Janus Henderson Treasury fund), you are getting legitimate yield from real assets with legal protections. The investment is in the fund, not in Centrifuge itself. If you are buying the CFG token, you are betting on future value accrual (fee distribution, governance upgrades) that has not materialized yet. The token currently captures $0 in protocol revenue. As of May 2026, CFG trades at $0.26 with a $150 million market cap and a 27x revenue multiple.

What does the CFG token actually do?

CFG is a governance and staking token. It lets holders vote on protocol upgrades and parameter changes. There is a staking mechanism. But there is no revenue sharing, no buyback, and no burn. The token has no claim on protocol fees or earnings. Holders Revenue on DefiLlama has been $0 every quarter since tracking began.

Is Centrifuge safe?

The platform has 21+ audits and uses SPV legal structures with KYC/AML compliance. For institutional investors, the legal protections are real. Credit risk exists in the lending pools (junior tranches absorb losses first). Smart contract risk exists across 10 blockchain networks. There have been no major hacks or protocol-level security incidents as of May 2026.

Centrifuge vs Ondo: which is better for RWA?

They serve different needs. Ondo focuses on tokenized Treasuries and yield products with a simpler interface and stronger retail brand ($3B+ market cap). Centrifuge is a broader toolkit that handles credit, CLOs, funds, and equities with deeper DeFi integration. If you want simple Treasury exposure, Ondo is more straightforward. If you are an asset manager launching a diversified tokenized fund with legal wrappers, Centrifuge offers more flexibility.

Centrifuge vs Maple Finance: what is the difference?

Maple is a pure institutional lending protocol with a cleaner revenue model and buyback mechanisms already in place. Centrifuge is broader (funds + credit + CLOs + equities) but captures less revenue per dollar managed. Maple reported $2.5M in quarterly protocol revenue in Q1 2026 on a smaller TVL base. For lending specifically, Maple has better unit economics. For diversified tokenized products, Centrifuge has more range.

Why is Centrifuge's TVL so high but market cap so low?

95% of the $1.57B TVL comes from two Janus Henderson funds. The TVL represents assets managed through the platform, not value captured by the protocol. Protocol revenue is only $5.5M annually on that $1.57B (0.35% take rate). The market is pricing CFG based on what the protocol actually earns, not on the headline TVL number.

Who uses Centrifuge?

518 unique holders as of May 2026. The dominant user is Janus Henderson through its Anemoy brand (Treasury fund, AAA CLO fund, S&P 500 fund). Other participants include Apollo-related products and various smaller credit originators. Coinbase has committed to using Centrifuge as preferred infrastructure on Base.

What is the Centrifuge token unlock schedule?

Team tokens (14% of supply) vest through March 2030. An additional 100 million tokens from governance proposal CP149 vest through April 2029. There is 3% annual inflation accruing to the treasury. Next significant unlock: July 14, 2026. Total supply is approximately 692 million CFG with roughly 580 million currently circulating.

Daniil Kozin structures tokenized real-asset deals in Europe and writes the RWA Roast series to cut through the conference slides. Previous roasts: Chainlink, Figure/Provenance, Stellar, Syrup, Ondo. Full archive at daniilkozin.com.

Sources: - DefiLlama: Centrifuge TVL ($1.571B), fees ($69.33M annualized), revenue ($5.51M), active loans ($78.66M), income statement Q3 2025 through Q2 2026, Holders Revenue ($0) - rwa.xyz: Distributed Asset Value ($1.56B), RWA Count (8), Holders (518), Monthly Transfer Volume ($1.71B), network breakdown by chain, individual asset market caps - CoinDesk: Coinbase strategic investment and preferred tokenization backbone announcement (May 5, 2026) - BusinessWire: Grove Basin launch with up to $1B daily liquidity commitment (May 14, 2026) - The Block: Sky $1B allocation to Janus Henderson via Grove infrastructure (June 2025 stealth launch) - Centrifuge docs (docs.centrifuge.io): Token summary, CP149 migration details, supply allocation, product architecture - CryptoRank / Tokenomist / DropsTab: Vesting schedules, team allocation (14%), inflation rate (3%), next unlock July 2026 - centrifuge.io: 1,768 assets tokenized, partnership claims - Maple Finance Q1 2026 reporting: $2.5M quarterly protocol revenue (for comparison)

Data as of May 17, 2026. RWA space moves fast. Always verify live metrics and do your own due diligence on credit pools.